{kind=link}

🇯🇵 Japan BoJ Macro — JGB Yields, Auctions & Policy Rates

Pricing

from $50.00 / 1,000 macro records

🇯🇵 Japan BoJ Macro — JGB Yields, Auctions & Policy Rates

Bank of Japan macro rates, JGB yield curve, MoF JGB auction calendar, money supply, FX reserves, and BoJ Policy Board monetary policy statements — JPY-denominated source-of-truth feed for Japan-rates desks, macro PMs, and AI-agent integrations.

Pricing

from $50.00 / 1,000 macro records

Rating

0.0

(0)

Developer

{kind=link}

Actor stats

0

Bookmarked

2

Total users

1

Monthly active users

4 hours ago

Last modified

Categories

Share

BoJ scatters Japan's monetary picture across three government sites: stat-search for the call rate and money stock, MoF for the JGB compound-yield CSV and auction calendar, and the Policy Board statement archive. This actor consolidates all of it into one normalized async pull — interest rates, the 1Y-to-40Y JGB curve, upcoming auctions, monetary base, FX reserves and Policy Board statement PDFs — so a Japan-rates desk replaces three terminal screens with a single structured feed back to 1974.

Built for Japan-rates desks, global macro PMs, JGB arbitrage traders, sovereign-debt analysts, and AI-agent integrations that need clean, structured Japan monetary data without paying $24K/yr for a Bloomberg terminal.

⚡ What you get

Per record (stable 8–12 fields depending on data_type):

| Field | Description |

|---|---|

data_type | One of interest_rates, jgb_yields, jgb_auctions, money_supply, fx_reserves, monetary_policy |

date | ISO observation date (YYYY-MM-DD) |

series_code | BoJ stat-search code (e.g. IR01'MADR1Z@D, FM01'STRDCLUCON) or constructed code (e.g. JGB_CME_10Y) |

series_name | Human-readable English name (e.g. "JGB compound-interest yield, 10Y") |

value | Numeric value (rate %, JPY amount, USD millions) |

unit | Unit string (% per annum, USD millions, 100 million yen, etc.) |

tenor | JGB tenor (2Y, 5Y, 10Y, 20Y, 30Y, 40Y) — JGB rows only |

issue | Auction issue description (e.g. 10-year, Liquidity Enhancement Auction) — auctions only |

auction_id | Stable per-auction key (e.g. JGB_2026-06-02_10Y) — auctions only |

stop_out_yield | Auction lowest accepted price — null until MoF publishes results |

bid_to_cover | Auction B/C ratio — null until MoF publishes results |

accepted_amount_JPY | Accepted amount in JPY — null until MoF publishes results |

statement_url | Direct PDF link — monetary policy rows only |

source_url | Source page on boj.or.jp or mof.go.jp |

fetched_at | UTC timestamp of the actor fetch |

🎯 Use cases

- Japan-rates desk — daily JGB curve + BoJ call rate + monetary base in one pull instead of three terminal screens.

- Pre-auction calendar feed — MoF publishes ~1 week ahead; size cash-curve trades around 5Y / 10Y / 20Y / 30Y supply.

- Sovereign-debt event studies — full historical JGB curve back to 1974/9/24 via

date_from=1974-09-24(the historical CSV). - RAG / AI macro agent — clean structured rows to answer "what did BoJ decide at the April 2026 MPM" with statement-PDF links, or "what's the latest 30Y JGB yield".

- Yen-cross desks — pair this actor with the MoF FX-intervention sibling for the rates → reserves → intervention chain.

- Research / academia — long-window stable BoJ time series (call rate back to 1998, basic loan rate back to 1882) for monetary-economics papers.

📊 Sample Output

👁 Japan BoJ Macro Rates + JGB Auctions sample

{kind=link}

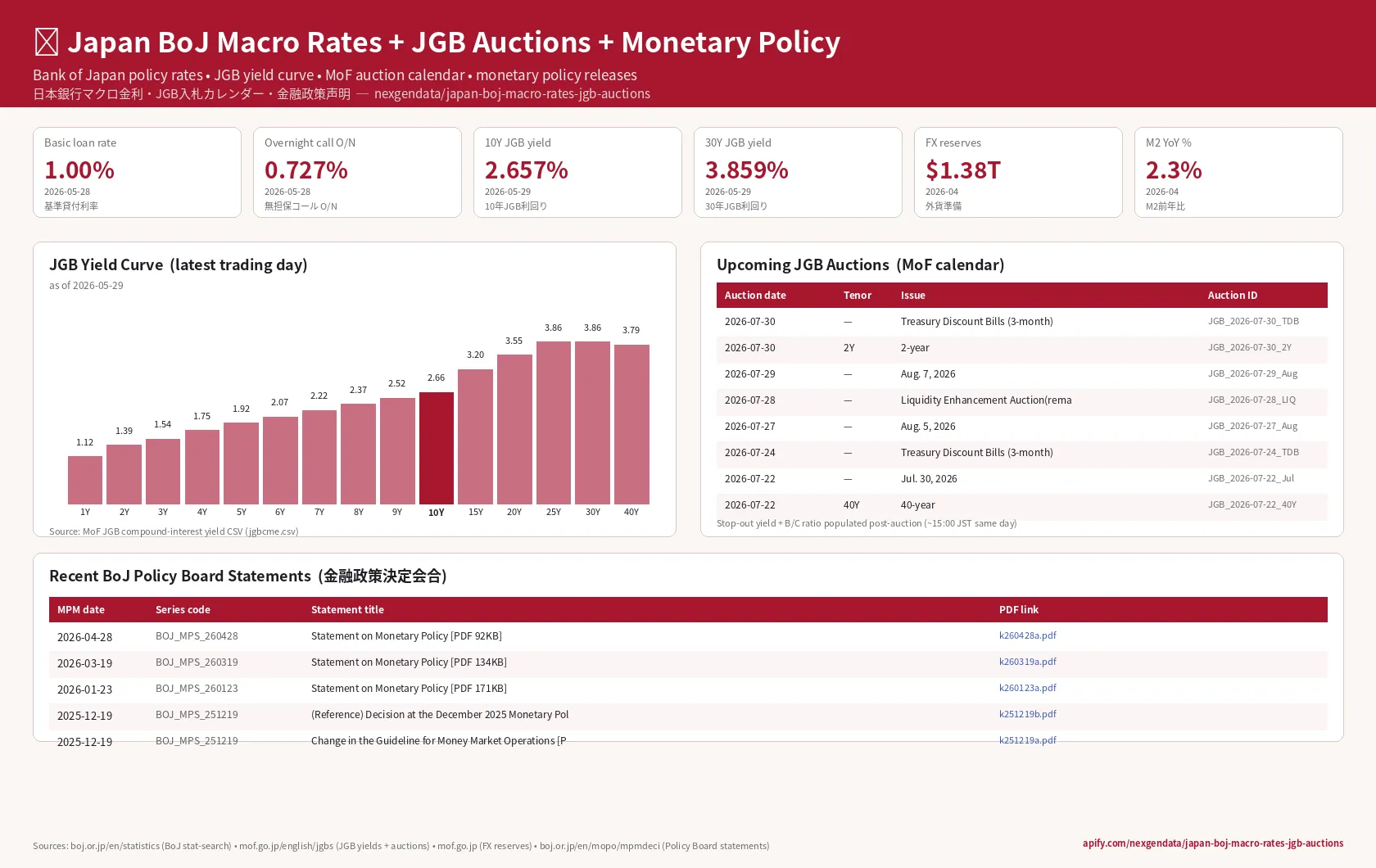

The dashboard renders the latest JGB yield curve (10Y headline), the BoJ basic loan rate (policy rate proxy), the call rate (overnight market rate), upcoming JGB auctions for the month, and recent Policy Board statement PDFs — all in one image with full Japanese terminology rendered in Noto Sans CJK JP.

A single jgb_yields row (data_type=jgb_yields, tenor_filter=10Y):

stop_out_yield/bid_to_cover/accepted_amount_JPYare present only onjgb_auctionsrows and are currently null — the actor surfaces the auction calendar, not the post-auction result PDFs.

🚀 How to use

Sample input — JGB 10Y yields, last 5 days (smoke):

Sample input — full Japan macro snapshot (default, 30-day window):

Sample input — JGB auction calendar for June 2026:

Python (apify-client):

cURL:

🇯🇵 日本語の説明

日銀政策金利・JGB利回り曲線・JGB入札カレンダー・マネーサプライ・外貨準備・金融政策決定会合声明を一括取得するAPIです。

主な用途

- 日本金利デスクのマクロPM — JGB曲線(1年〜40年)・無担保コール O/N・マネタリーベースを1回の非同期コールで取得。

- JGB入札裁定 — 財務省が約1週間前に公表する入札カレンダーをフィードとして取得。5年・10年・20年・30年の発行サイズを事前に把握。

- 国債アナリスト — 1974年9月24日以降のJGB利回り完全履歴を

date_from=1974-09-24で取得可能。 - AIマクロエージェント — 「2026年4月の金融政策決定会合で日銀は何を決定したか」「最新の30年JGB利回りは」などのRAG質問にクリーンな構造化データで答える。

- 円クロスFXデスク —

japan-mof-fx-intervention-trackerと組み合わせて、JPY政策の全体像(金利→準備→介入)を取得。 - 研究・学術用途 — 長期間にわたる安定したBoJ時系列(コールレートは1998年〜、基準貸付利率は1882年〜)。

入力パラメータ

data_type— 取得データタイプ(金利/JGB利回り/入札/マネーサプライ/外貨準備/金融政策/全て)series_filter— BoJ時系列コード絞り込み(例:IR01,FM01,MD02)tenor_filter— JGB残存期間絞り込み(2Y,5Y,10Y,20Y,30Yほか)date_from/date_to— 観測日範囲(ISO 8601)max_records— 最大レコード数(1〜1000、既定値100)

データソース

- 日本銀行

https://www.boj.or.jp/en/statistics/およびhttps://www.stat-search.boj.or.jp/ - 日本銀行金融政策決定会合声明

https://www.boj.or.jp/en/mopo/mpmdeci/ - 財務省JGB入札カレンダー

https://www.mof.go.jp/english/policy/jgbs/auction/calendar/ - 財務省JGB金利情報

https://www.mof.go.jp/english/policy/jgbs/reference/interest_rate/ - 財務省外貨準備等の状況

https://www.mof.go.jp/policy/international_policy/reference/official_reserve_assets/

質問: hello@thenextgennexus.com

⚖️ Legal & data sources

- Bank of Japan time-series statistics are published under the BoJ Open Data convention (English + Japanese mirrors). No license required for programmatic access; attribution requested.

- Bank of Japan Monetary Policy Releases (Policy Board statements) are public open-data published immediately after each MPM (Monetary Policy Meeting) under BoJ Act Article 15.

- MoF JGB auction calendars and yield CSVs are Ministry of Finance open-data published under Japan's Public Records and Archives Management Act and the Government Bond Act.

- MoF International Reserve Assets are published monthly per IMF SDDS (Special Data Dissemination Standard) commitments.

All requests are issued with a polite identified User-Agent (NexGenData BoJ Macro Actor (hello@thenextgennexus.com)), follow upstream rate limits, and observe robots.txt. No authentication is required for any source; no scraping of restricted, paywalled, or auth-walled content.

❓ FAQ

Q: Which is the "policy rate" — basic loan rate or call rate?

A: BoJ targets the uncollateralized overnight call rate as its operational policy rate; the basic loan rate (旧公定歩合) is the standing-facility ceiling. Pull data_type: "interest_rates" to get both side-by-side.

Q: Why are auction result fields null?

A: Only the auction calendar (date + issue type) is fetched, published up to a week in advance. Auction results (price, yield, B/C ratio, accepted amount) are released ~3 PM JST on the auction day via a separate PDF and are not yet parsed — so stop_out_yield, bid_to_cover and accepted_amount_JPY are null.

Q: How far back does the JGB curve go?

A: To 1974 via the historical CSV (date_from=1974-09-24). The actor pulls the current-month CSV for windows ≤30 days and falls back to the 1974~ historical CSV for longer windows.

Q: How current is the data? A: JGB yields are next-trading-day; the call rate updates daily ~2 PM JST; money stock & FX reserves are monthly; Policy Board statements drop immediately post-MPM.

Q: How do I get only the 10Y JGB yield?

A: {"data_type": "jgb_yields", "tenor_filter": "10Y"}. The actor filters to a single tenor and pushes one row per trading day.

Q: BoJ vs FRED — should I use this or the FRED actor? A: FRED carries Japan rate series but is US-Treasury-first and lags BoJ's primary feed by hours (sometimes days for monthly releases). FRED also has no JGB auction calendar and no MoF FX reserves. Use this actor for source-of-truth Japan macro.

🔗 Related Actors

Part of the NexGenData APAC macro / central-bank cluster — composable into any cross-border macro, FX or rates workflow:

- 🇹🇼 Taiwan CBC Macro + FX Rates — Bank of Taiwan daily TWD FX matrix + CBC policy rate, money supply and reserves.

- 💴 Japan MoF FX Intervention Tracker — MoF yen-intervention record back to 1991, parsed from the FEIO CSV.

- 🇰🇷 Korea BoK Monetary Policy + ECOS — Bank of Korea ECOS wrapper: base rate, CPI, M1/M2, GDP, FX reserves, trade balance.

- 🇮🇳 India RBI Monetary Policy Statements — RBI MPC repo-rate decisions, stance, CRR/SLR and forecasts as structured rows.

- 🇹🇼 Taiwan Customs Export Trade Data — Taiwan export / import / trade-balance data by partner country and HS code.

🏷️ About NexGenData

NexGenData operates a fleet of public-data actors covering global capital markets, regulatory filings, macro statistics, IP databases, and corporate registries. We specialize in turning fragmented government open-data into clean structured JSON for traders, analysts, and AI agents.

Contact: hello@thenextgennexus.com

Fleet: apify.com/nexgendata?fpr=2ayu9b

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}