The United States announced its reciprocal tariff policy on 2 April 2025. This marks the most significant shift in US trade policy since the establishment of the North American Free Trade Agreement (NAFTA) in 1994 and, arguably, the most impactful global trade policy change since the establishment of the General Agreement on Tariffs and Trade (GATT) in 1947. The global reaction, from economic analysts to financial markets, has been overwhemingly negative.

Beyond the immediate concerns about the economic effects of these tariffs, the reciprocal measures are indicative of a broader trend towards a more isolationist US policy and a gradual detachment from global cooperation and the international economy. Discriminatory policies aimed at boosting US industry have been pursued since the previous Trump administration and have continued and expanded during the Biden administration. The Biden government maintained and intensified measures that reduced the extent of US global cooperation. Furthermore, the US has consistently blocked the appointment of judges to the World Trade Organization (WTO) Appellate Body during both the Trump and Biden presidencies.

Having said this, the newly implemented reciprocal tariffs, given their anticipation, magnitude, clumsy implementation and weak economic foundations, top the list of any previous US actions in isolating its economy (and society) from the rest of the world. No prior policy comes close to this poorly crafted and designed measure. In fact, if we compound the effect of the reciprocal tariffs with the virtual elimination of US development assistance, this policy represents one of the most severe blows to the least powerful countries and most vulnerable populations.

What are reciprocal tariffs?

The new policy introduces two sets of tariffs applicable to different groups of countries: a general or base tariff and a reciprocal tariff linked to the US trade deficit with a specific country. The general tariff, set at 10% will be applied to imports from all countries (except Canada and Mexico) starting on 5th April (Sec3, a of the Executive Order). For example, if the Most Favored Nation (MFN) tariff on men’s cotton shorts was 8.9% (HS 620342), the total duty to pay under the new regime would be 18.9% (MFN+10%). Notably, countries with existing free trade agreements with the US will still be subject to this base tariff.

In addition, according to Sec 3 a, countries listed under Annex I will be subject to a bespoke reciprocal, effective 9thApril. These tariffs are supposedly designed to account for the perceived implicit ‘duty’ applied to US products in those countries. Most trade specialists are baffled by the methodology used to calculate these tariffs.

The primary basis for calculating country-specific reciprocal tariffs is the extent of the US goods trade deficit with that nation. The underlying assumption behind these “reciprocal” tariffs is that a US trade deficit with partner countries is a direct consequence of their respective national trade policies. This view incorrectly attributes the trade balance solely to a partner's tariffs, and other factors such as monetary measures (e.g., currency manipulation), non-tariff trade barriers and even domestic consumption taxes (e.g., VAT). The reciprocal tariff, according to the Trump administration’s view, is intended to provide some compensation for this perceived damage (the US, according to their calculations and assessment, has been very lenient and just compensates, arbitrarily set, at half of the supposed harm). Like the base tariff, the reciprocal is applied in addition to existing MFN or preferential tariffs.

The reciprocal tariff varies significantly across countries. However, due to their productive structures and other reasons not well understood by President Trump’s advisors, it disproportionately impacts goods produced by Asian countries. This outcome is not surprising. Countries such as Bangladesh, Vietnam or Cambodia have a relative abundance of manual labour and consequently specialise in the production and trade of goods intensive in this resource (e.g. garments and footwear). The US, in contrast, with its relative abundance of land, capital and high-skilled labour, specialises in the production of high-tech products (e.g. aircraft engines). The economies of the US and these Asian countries can be described as ‘complementary’, each specialising in their respective areas of comparative advantage. The US imports a significant volume of goods from these countries because they can produce them at a lower cost.

As a result of the reciprocal duties, imports originating in Bangladesh, for instance, will be subject to an additional 37% tariff. Consequently, men’s cotton shorts produced in Bangladesh will be subject to a total duty of 45.9%. Table 1, in the annex, illustrates the combined effect of the new reciprocal and base tariffs alongside the MFN and the effectively applied duty (this includes the incidence of trade agreements and preferences).

The impact in the US

There will be an immediate fiscal impact from these duties. Rough calculations, considering the announced and applied duties on US imports (excluding Mexico and Canada), suggest an additional tariff revenue of approximately $540 billion. However, three key factors need consideration that will affect the value on what the new tariffs is applied to. First, the quantities of imported goods are likely to decrease to varying degrees depending on the product, due to the price increases (economists refer to this as the price elasticity of demand). Second, given the US’s is a large country and represents a significant share in global trade, exporters to the US may be compelled to lower their prices. Third, if the generalised rise in prices leads to a fall in real incomes, there will also be an income effect, further reducing demand. Therefore, the ultimate impact on total tariff revenue will depend on the interplay of these three forces, which are likely to reduce the initial revenue projection. Regardless of these fiscal impacts, US consumers will ultimately bear the cost through higher prices, effectively contributing to fund the promised reduction in the corporate tax.

Proponents of this measure expect an additional expected benefit: the return of industries that previously left the US or offshored their production due to partners’ trade policies and what they consider poor judgment by previous administrations. Behind this assumption is the idea that firms seeking to avoid the burden of the new tariffs will relocate their production back to the US (this is frequently called tariff-jumping investment). This simplistic view envisions a rapid expansion of steel mills, banana plantations, car factories, and low-productivity garment workshops within the US, without considering other crucial factors. This scenario appears implausible and undesirable for the US population, who would likely benefit more from specialising in activities intensive in capital and high-skilled labour, such as aircraft engines, where these resources can be used more productively.

While the US boasts a large economy with abundant natural, capital and human resources, there are limits to the number of reshored industries it can support. Industries protected by tariffs will begin to compete for resources, particularly capital and, crucially, labour. These reshored industries will not only race other entrants to hire from a limited pool of available workers (given the very low unemployment rate in the US) but also with incumbent firms in both manufacturing and services sectors. So, the question then becomes how these increasingly scarce workers will be allocated. It is plausible that some high-tech and automotive industries might onshore production. However, it is highly unlikely that industries intensive in manual labour will return to the US. Effectively, sectors such as garments, footwear, toys and labour-intensive agriculture are likely to remain globally dispersed. nevertheless, as we will see, the specific implementation of these tariffs may significantly influence the future location of this production.

How is the rest of the world affected?

An initial approach to assessing the global impact of the announced tariffs involves examining their effect on specific products. Table 1 presents the weighted applied tariffs (AHS), which account for both MFN and preferential duties, alongside the final duty after the implementation of the new reciprocal tariffs. The table is sorted by the difference between these two tariff levels to highlight the jump in duties. The presented data covers the first 20 chapters and reveals considerable variation across different product categories. As the data indicates, the new duties primarily target footwear, garments and light manufacturing goods. These are typically sectors prevalent in countries with a relatively large manual labour force. Notably, as will be further discussed, these are the product categories are predominantly manufactured in Asian countries. The share of the US in total global demand for many of these products is very high, anticipating significantly global impact in these markets and, of course, in the countries where these products represent a significant share of their exports.

Furthermore, an understanding of the tariffs’ impact can be gained by comparing the level of the newly applied tariffs with each country’s export reliance on the US market. Countries such as Cambodia, Vietnam and Sri Lanka will face substantial duties, and the US accounts for over 25% of their exports.

However, the impact will be more complex, with two additional dimensions to consider. First, as mentioned earlier, US consumers and producers will reduce their demand for these products due to price and income elasticity. Ultimately, US consumers will bear the cost of these measures. Second, the treatment of different countries has been uneven, with some significantly affected while others have received more lenient treatment. While Asian countries like Bangladesh, Cambodia, Sri Lanka and Vietnam will face the highest tariffs, many countries in Africa and Latin America will be only subject to the base duty. This disparity in duties is likely to have significant distributional consequences.

Consider the example of men’s cotton shorts again. Countries such as Ethiopia, Kenya and Tanzania have benefitted from preferential duty access to the US market under the African Opportunities Growth Act (AGOA). In contrast, Bangladesh faced an 8.9% MFN duty rate. This created an advantage for African exporters. Even though Bangladesh is a more efficient supplier, African countries managed to secure a certain market share in the US. Moreover, in Central America, Nicaragua has captured a significantly larger portion of the market thanks to preferential access provided by the Dominican Republic-Central America Free Trade Agreement.

The new tariffs will widen the differential between duty rates. Table 2 compares the rates for most Asian exporters affected by the reciprocal tariffs with those of other non-Asian exporters. The new tariffs increase the differentials for almost all non-Asian partners, with the exception of Lesotho. Even if AGOA is not renewed and African countries begin paying MFN duties, the differential for countries like Kenya or Madagascar compared to Cambodia, for example, could be as high as 30%.

Although the tariffs, both base and reciprocal, will reduce overall US demand, the countries facing the largest increases will bear the brunt of the adjustment. A significant part of this adjustment will involve a substitution away from the countries with higher duties towards countries such as Kenya and Nicaragua, leading to a substantial reduction in imports from more traditional exporters. For US consumers, this trade-diverting effect away from more efficient suppliers represents a clear welfare loss.

Table 2: Differential duties (after imposing the new US reciprocal tariffs) between exporters to the US of men’s cotton shorts

The impact and responses in countries around the world

So, what options do affected countries have? They can essentially do three things:

1. Retaliate – responding to economic self-harm with further economic self-harm

This would involve increasing duties and taxes on US products (and potentially services) to counteract the impact of the US tariff. This approach would be economically painful, as it applies the same harmful principles that underlie the US reciprocal tariffs’ impact on US consumers. Of course, the magnitude of the impact on US exporters would depend on the size of the retaliating economies. Only large entities such as the EU, India or China could significantly affect the demand for US exports. Nevertheless, the US could increase even further these tariffs of Commerce and the United States Trade Representative (USTR) to increase or expand in scope of the tariffs in case of retaliation).

However, politically, retaliation is unlikely to be effective given the current prominence of tariffs in US policy. It is improbable that the current administration would withdraw these new tariffs, as it would be seen as a significant defeat (though this does not exclude the possibility of some adjustments). Furthermore, there would be concerns that the US could escalate its measures even further with specific tariffs applied to critical sectors such as pharmaceuticals and semiconductors. In another words, it is something that the US must go through.

For most other countries, in addition to the substantial economic costs, retaliation would be directly ineffective. Therefore, it is best avoided.

2. Re-orient exports and find new partners

Countries such as Bangladesh or Sri Lanka, facing reduced demand from the US, can explore and seek alternative customers. This is not a simple task, as it requires significant information gathering and often costly efforts to engage with new buyers in different markets. However, in principle, it is possible to redirect some production to other markets. The feasibility of this, of course, depends on the absorption capacity of the rest of the world and can vary considerably across products.

The negotiation of trade agreements with other countries can provide relief for the affected and opportunities in other sectors. The implementation of agreements such as the African Continental Free Trade (AfCFTA) and the EU-Mercosur Association Agreement needs to be accelerated, not only to address this immediate crisis but also to reinforce the global commitment to free trade and integration. In virtue of the discussion, finalising the negotiations on rules of origin for textiles and garments in the AfCFTA is critical. The negotiation of other trade agreements, such as the India-Sri Lanka FTA, need to be concluded as soon as possible under these circumstances.

However, in the short run, fierce global competition is likely as firms seek new customers, potentially leading to a race to the bottom in pricing. Nevertheless, countries now have an incentive to forge closer relationships amongst themselves (excluding the US)

3. Negotiate with the US

Section 4 of the EO grants the Secretary of Commerce and the USTR the authority to decrease or limit the scope of the duties if a trading partner takes steps to remedy non-reciprocal trade arrangements and align sufficiently with the US on economic matters. This opens a window for y for countries to reduce their MFN duties (or other taxes) to appease the US and potentially secure a lower tariff.

Countries such as Bangladesh or Fiji, which currently have relatively high MFN duties, might consider reducing these tariffs to encourage the US to lower the reciprocal duties imposed on them. The impact of such a move on consumers would depend on its implementation. A generalised reduction of MFN tariffs will benefit consumers in Bangladesh. However, a reduction applied solely to US imports, on top of not being in the spirit of the non-discrimination principle, could lead to trade diversion away from more efficient suppliers.

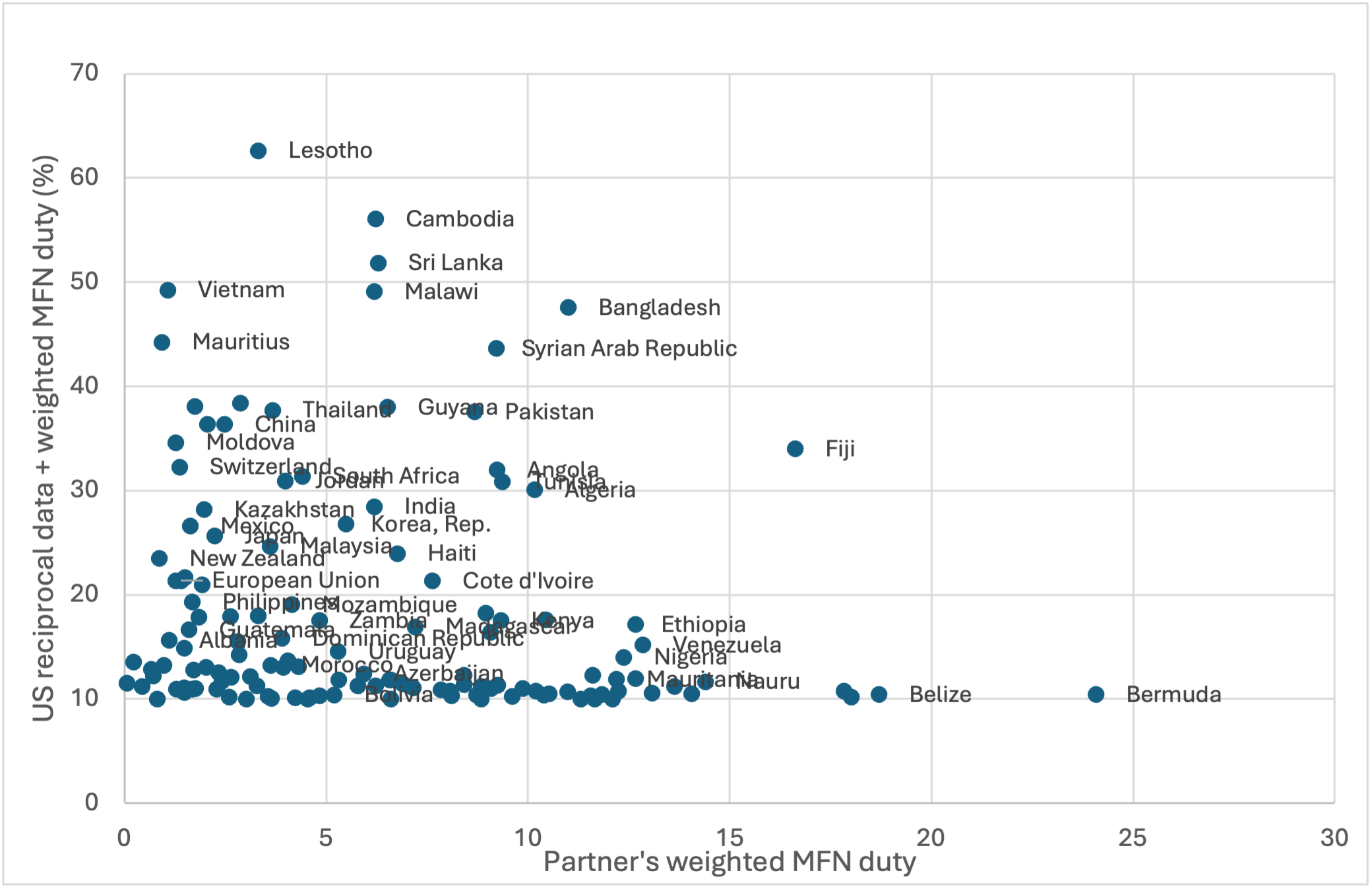

However, the correlation between a higher existing duty and a higher reciprocal duty imposed by the US is not consistently clear. Figure 2 compares the new US tariffs (added to the existing weighted MFN duty) with the weighted MFN duty applied by the partner country. While Fiji, Bangladesh and Sri Lanka might potentially benefit from reducing their duties, it remains uncertain what actions Lesotho could take to appease the US Government and secure a reduction in its imposed duty.

Figure 2: The relationship between reciprocal tariffs and the partner tariff

{kind=link}

Behind the introduction of reciprocal duties are flawed assumptions and premises about international trade. It contradicts over 200 years of accumulated knowledge in trade policy, macroeconomics, industrial policy and related fields. Trade deficits are not solely determined by the policies of individual countries but arise from a complex combination of consumer preferences, technological advancements and resource endowments on the trade side. Furthermore, as we have seen earlier in our example, global monetary and fiscal policies and the interactions with various institutions, including US entities like the Federal Reserve, play a significant role.

The implementation of these reciprocal tariffs makes a combination of inflation and recession in the US highly probable. This inevitable outcome will likely force voters to confront the reality of this damaging economic policy. The US government may eventually recognise the error and reverse these policies. Unfortunately, until that time, the primary course of action for other countries is to exercise patience and continue to foster trade relationships among themselves to mitigate the void created by Trump.

In fact, drawing upon the theories of David Ricardo, unfortunately ignored by Trump and the masterminds behind these policies, this situation presents an opportunity for the rest of the world to expand trade even further and build a larger, more integrated global economy. The US will, in time, likely rejoin this trajectory.