|

VOOZH | about |

|

VOOZH | about |

The movement of cash & cash equivalents or inflow and outflow of cash is known as Cash Flow. Cash inflows are the transactions that result in an increase in cash & cash equivalents; whereas, cash outflows are the transactions that result in a reduction in cash & cash equivalents. Hence, a statement showing flows of cash & cash equivalent during a specified time period is known as a Cash Flow Statement. One can prepare a cash flow statement if the two comparative balance sheets of a company are given. The transactions of a cash flow statement are categorised into three activities; namely, Cash flow from Operating Activities, Cash flow from Investing Activities, and Cash flow from Financing Activities. The Institute of Chartered Accountants in India has issued Accounting Standard AS - 3 revised for the preparation of cash flow statements. Besides, with the introduction of the Companies Act 2013, the preparation of a Cash Flow Statement is now mandatory for every type of company except OPC (One Person Company) [Section 2(40)].

The sale and purchase of investments and fixed assets, which are not held by a company for resale purposes are covered under Investing Activities. Cash flow from investing activities also discloses the expenditures incurred for the resources intended to generate future income and cash flows of the company. Some examples of cash flows arising from investing activities are as follows:

Calculate Cash flow from Investing Activities from the following information:

Additional Information:

1. Interest Received on debentures held as investment ₹5,000

2. Dividend paid on Equity Shares ₹30,000

3. Dividend received on Shares held as investment ₹40,000

4. Interest paid on debentures issued ₹12,000

5. The firm also purchased land out of the surplus funds for investment purposes and was let out for commercial use. Rent received for the same was ₹50,000

Note: We will not record Interest Paid (₹12,000) and Dividend Paid (₹30,000) in Cash flow from Investing Activities. It will be recorded in Cash flow from Financing Activities.

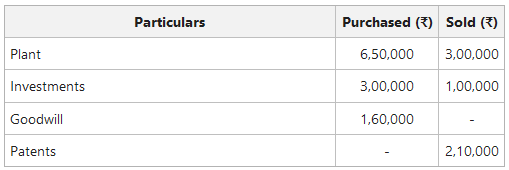

Calculate Cash Flow from Investing Activities from the following information:

Additional Information:

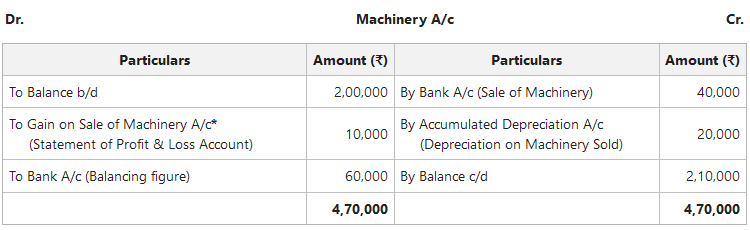

1. During the year, a machine costing ₹50,000 with accumulated depreciation of 20,000 was sold for ₹40,000.

2. Patents written off were ₹30,000, and some patents were sold at a profit of ₹10,000.

Working Note 1:

*Gain on Sale of Machinery = Sale Price - Book Value of Machinery

= ₹40,000 - ₹30,000 (₹50,000 - ₹20,000)

= ₹10,000

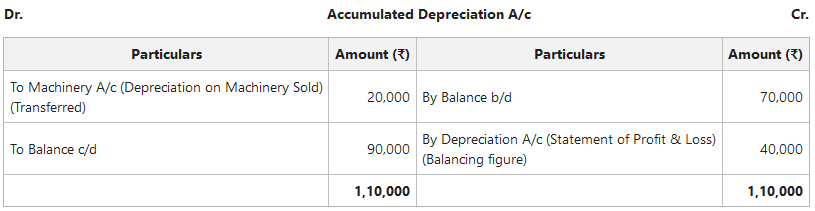

Working Note 2:

Working Note 3:

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}