|

VOOZH | about |

|

VOOZH | about |

The movement of cash & cash equivalents or inflow and outflow of cash is known as Cash Flow. Cash inflows are the transactions that result in an increase in cash & cash equivalents; whereas cash outflows are the transactions that result in a reduction in cash & cash equivalents. Hence, a statement showing flows of cash & cash equivalent during a specified time period is known as a Cash Flow Statement. One can prepare a cash flow statement if the two comparative balance sheets of a company are given. The transactions of a cash flow statement are categorised into three activities; namely, Cash flow from Operating Activities, Cash flow from Investing Activities, and Cash flow from Financing Activities. The Institute of Chartered Accountants in India has issued Accounting Standard AS - 3 revised for the preparation of cash flow statements. Besides, with the introduction of the Companies Act 2013, the preparation of a Cash Flow Statement is now mandatory for every type of company except OPC (One Person Company) [Section 2(40)].

A cash flow statement is prepared under three parts; viz., Part A, B, and C.

Part A includes Cash Flow from Operating Activities

Part B includes Cash Flow from Investing Activities

Part C includes Cash Flow from Financing Activities

Cash Flow Statement

For the year ended 31st March 20XX

(AS-3 Indirect Method)

Particulars | ₹ | ₹ |

|---|---|---|

| 1. Cash Flow from Operating Activities: | ||

| Profit & Loss Appropriation Account (Current Year) | XXXX | |

| Less: Profit & Loss Appropriation Account (Previous Year) | (XXXX) | XXXX |

| Add: Proposed Dividend for the Current Year | XXXX | |

| Add: Interim Dividend Paid during the Current Year | XXXX | |

| Add: Transfer to Reserve | XXXX | |

| Add: Provision for Tax made during the Current Year | XXXX | |

| Less: Refund of Tax credited to Profit & Loss Account | (XXXX) | |

| Less: Extraordinary Item (if any) credited to Profit & Loss Account (i.e., Insurance proceeds from earthquake disaster settlement) | (XXXX) | |

Net Profit before Taxation and Extraordinary Items | XXXX | |

| Adjustment related to Non-cash and Non-operating Items: | ||

| Add: Depreciation on Fixed Assets | XXXX | |

| Interest on Borrowings | XXXX | |

| Preliminary Expenses/Underwriting Commission/Discount on Issue of Debentures/Shares Written-off | XXXX | |

| Goodwill/Patents/Trade Marks/Copyright Amortised | XXXX | |

| Loss on Sale of Machinery, Land and Building, Investments, etc. | XXXX | |

| Premium Payable on redemption of Preference Shares/Debentures | XXXX | XXXX |

| Less: Interest Income | (XXXX) | |

| Dividend Income | (XXXX) | |

| Discount on redemption of Preference Shares/Debentures | (XXXX) | |

| Profit on Sale of Machinery, Land and Building, Investments, etc. | (XXXX) | (XXXX) |

Operating Profit before Working Capital Changes | XXXX | |

| Adjustments related to Change in Current Assets and Current Liabilities: | ||

| Add: Decrease in Current Assets and Increase in Current Liabilities: | XXXX | |

| Decrease in Stock | XXXX | |

| Decrease in Trade Receivables (Debtors and Bills Receivable) | XXXX | |

| Decrease in Prepaid Expenses | XXXX | |

| Decrease in Accrued Income | XXXX | |

| Increase in Trade Payables (Creditors and Bills Payable) | XXXX | |

| Increase in Outstanding Expenses | XXXX | |

| Increase in Income Received in Advance | XXXX | XXXX |

| Less: Increase in Current Assets and Decrease in Current Liabilities: | (XXXX) | |

| Increase in Inventories (Stock) | (XXXX) | |

| Increase in Trade Receivables (Debtors and Bills Receivable) | (XXXX) | |

| Increase in Accrued Incomes | (XXXX) | |

| Increase in Prepaid Expenses | (XXXX) | |

| Decrease in Trade Payables (Creditors and Bills Payable) | (XXXX) | |

| Decrease in Outstanding Expenses | (XXXX) | |

| Decrease in Advanced Incomes | (XXXX) | (XXXX) |

Cash generated from Operations | XXXX | |

| Less: Income Taxes paid (Net of Refund) | (XXXX) | |

Cash Flow from Extraordinary Items | XXXX | |

| Less: Extraordinary Items | (XXXX) | |

Net Cash Inflow/Outflow from Operating Activities | XXXX | |

| 2. Cash Flow from Investing Activities: | ||

| Add: Proceeds from Sale of Machinery/Land and Building | XXXX | |

| Add: Proceeds from Sale of Investments | XXXX | |

| Add: Proceeds from Sale of Patents/Trade Marks/Copyrights | XXXX | |

| Add: Rent/Dividend/Interest Received | XXXX | |

| Less: Purchase of Machinery/Land and Building | (XXXX) | |

| Less: Purchase of Investments | (XXXX) | |

| Less: Purchase of Patents/Trademarks/Copyrights/Goodwill | (XXXX) | XXXX |

Net Cash Inflow/Outflow from Investing Activities | XXXX | |

| 3. Cash Flow from Financing Activities: | ||

| Add: Proceeds from Insurance of Share Capital | XXXX | |

| Add: Proceeds from Long-term Borrowings | XXXX | |

| Less: Redemption of Preference Shares/Buy-back of Equity Shares | (XXXX) | |

| Less: Repayment of Borrowings | (XXXX) | |

| Less: Interest Paid on Borrowings | (XXXX) | |

| Less: Interim Dividend Paid | (XXXX) | |

| Less: Final Dividend Paid | (XXXX) | XXXX |

Net Cash Inflow/Outflow from Financing Activities | XXXX | |

| 4. Net Increase (Decrease) in Cash and Cash Equivalent [1 + 2 + 3] | XXXX | |

| 5. Add: Cash and Cash Equivalent at the beginning of period (Cash in Hand + Cash at Bank + Marketable Securities/Short-term Deposits) | XXXX | |

| 6. Cash and Cash Equivalent at the end of period [4 + 5] (Cash in Hand + Cash at Bank + Marketable Securities/Short-term Deposits) | XXXX |

Note: The Cash Flow Statement of a Company will not include Issue of Shares/Debentures for consideration other than cash and purchase of a Non-current Asset against the issue of Shares/Debentures because these transactions do not involve any inflow/outflow of cash.

Prepare a Cash Flow Statement of Gaurav Ltd. on the basis of the information given in the Balance Sheet:

Note: It is assumed that the Debenture Interest is paid during the year & Redemption is made at the end of the year.

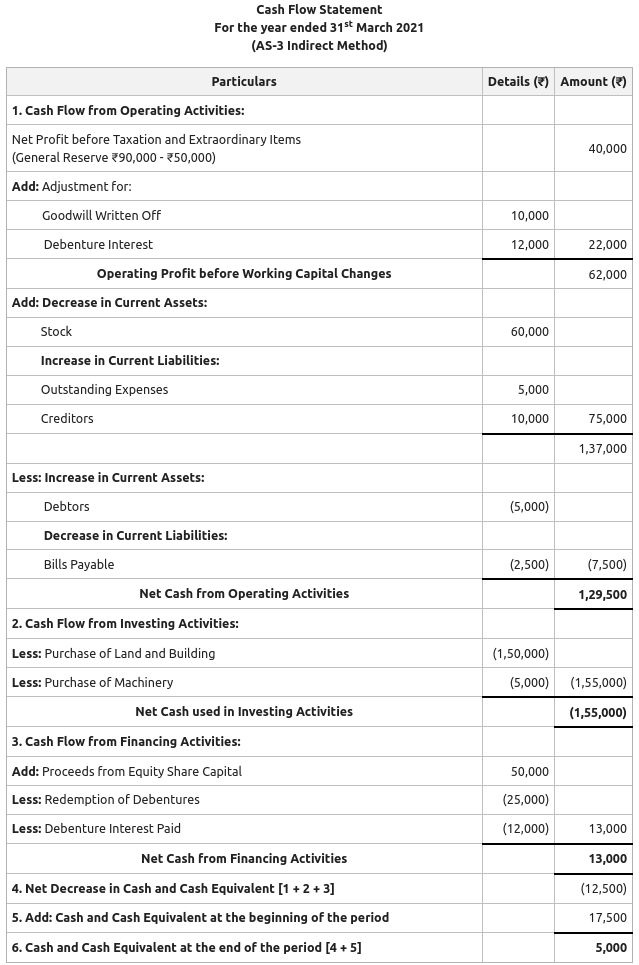

From the information given in the following Balance Sheet of Kashish Ltd. as on 31st March 2021, prepare its Cash Flow Statement:

Notes to Accounts:

Additional Information:

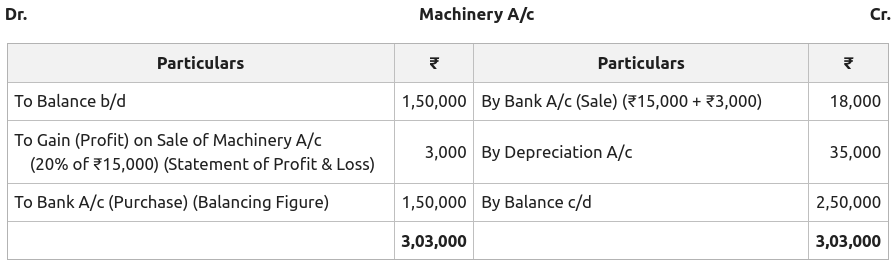

1. Machinery costing ₹50,000 on which depreciation charged was ₹35,000 was sold at a profit of 20% on book value. Depreciation charged during the year was ₹35,000.

2. Preference Shares were redeemed at par on 31st March 2021.

3. Equity Shares were issued on 1st April 2020, and Debentures were redeemed on 1st January 2021.

4. The company declared and paid an interim dividend on Equity Shares @ ₹20 per share out of General Reserve. It did not propose final dividend on Equity Shares.

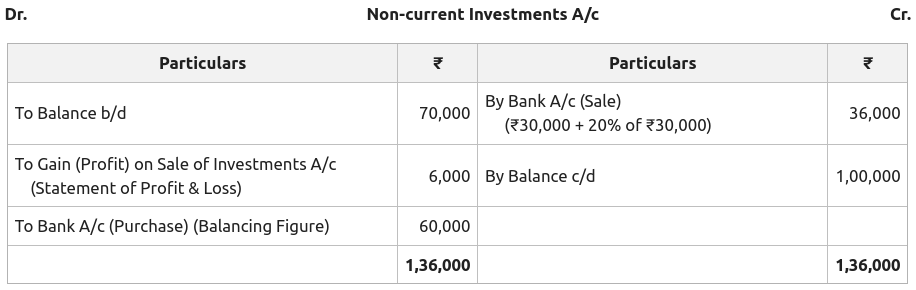

5. Non-current Investments costing ₹30,000 were sold at a profit of 20%.

6. Income Tax ₹22,500 was provided.

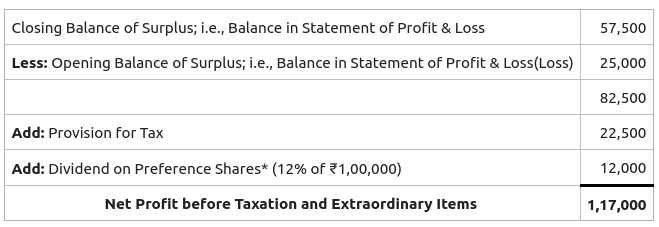

1. Net Profit before Taxation and Extraordinary Items:

*i) The interim dividend on equity shares is paid out of General Reserve, instead of appropriated out of Surplus; i.e., Balance in Statement of Profit & Loss. Therefore, it is not included while calculating Net Profit before Taxation and Extraordinary Items. However, Preference Dividend is appropriated out of Surplus. Therefore, it is included while calculating Net Profit before Taxation and Extraordinary Items.

ii) Dividend to shareholders of Preference Shares is paid if the dividend is paid on Equity Shares. Kashish Ltd. has not proposed its final dividend on Equity Shares but has paid interim dividend on Equity Shares. Therefore, it should pay dividends on Preference Shares.

2. Provision for Tax:

3. Machinery:

4. Non-current Investments:

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}