|

VOOZH | about |

|

VOOZH | about |

A debenture is a written instrument or document issued by a company acknowledging a debt borrowed from investors and specifying the terms of repayment of the principal amount along with the payment of interest at a predetermined rate. It serves as evidence of the company's obligation to repay the borrowed funds and is commonly used as a source of long-term finance. According to Section 2(30) of the Companies Act, 2013, “Debenture includes debenture stock, bonds and any other instrument of the company evidencing a debt, whether constituting a charge on the assets of the company or not.” According to Topham, “A debenture is a document given by a company as evidence of a debt to the holder usually arising out of a loan and most commonly secured by a charge.” The person to whom debentures are issued is known as a debenture holder, who acts as a creditor of the company and is entitled to receive interest and repayment of the principal amount as per the terms of issue.

A listed company can go for the issue of debentures for public subscription, but an unlisted company cannot issue debentures to the public in general. However, by private placement, both listed and unlisted companies may issue debentures. The accounting entries and procedures for issuing debentures are similar to that for the issue of shares. Debentures may be issued for cash; consideration other than cash; and as collateral security. Debentures may be issued at par; premium; or at discount whether issued for cash or consideration other than cash.

Debentures can be issued at par or premium when issued at cash.

1. Issue of Debentures at Par:

When debentures are issued at their nominal (face) value, it is known as Debentures issued at Par. For example, Debentures of a nominal (face) value of ₹200 are issued at ₹200.

1. On receipt of application money:

2. On transfer of application money to Debenture A/c:

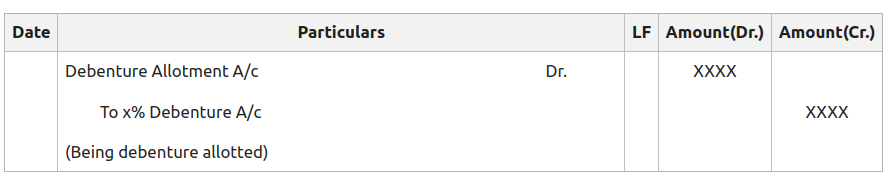

3. On allotment due:

4. On receipt of allotment money:

5. On due of call money:

6. On receipt of call money:

Illustration 1.

Jimmy Ltd. issued 10,000; 12% Debenture of ₹ 100 each payable on application by 1st April 2022 at par, payable 20 on application, 30 on the allotment, and the balance on the first and final call. All money due was duly received.

Pass the Journal entries in the books of the company.

Solution:

2. Issue of Debentures at Premium:

When debentures are issued at a price that is higher than their nominal (face) value, it is known as Debentures issued at Premium. For example, Debenture of nominal (face) value of Rs. 200 issued at Rs. 225, means debentures are issued at a premium of Rs.25. The premium received is credited to Securities Premium Account, and can be utilised for the purposes specified in Section 52(2) of the Companies Act, 2013.

The entry for Debentures issued at Premium will be (If the premium is included in allotment):

Note: All other entries will be the same as PAR.

Illustration 2.

A company issued 2,000, 10% debentures of ₹ 100 each at ₹ 110 payable as follows:

₹ 20 on application

₹ 40 on allotment (including premium of ₹ 10)

₹ 50 on first and final call

All the debentures were applied for and allotted. All money due was received. Pass the necessary Journal Entries.

Solution:

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}