|

VOOZH | about |

|

VOOZH | about |

A Provision in accounting is generally some set aside profits to be used under specific contingencies. They are the reserves that are being made for specific situations and are to be compulsorily used in those conditions only. A provision is seen as an upcoming liability and should not be treated as savings. Provisions journal entry is passed to show the amount set aside by the firm to meet contingencies.

Journal Entry:

5% Provision for bad debts is to be maintained against the bad debts on debtors amounting to ₹50,000. Record the necessary journal entry.

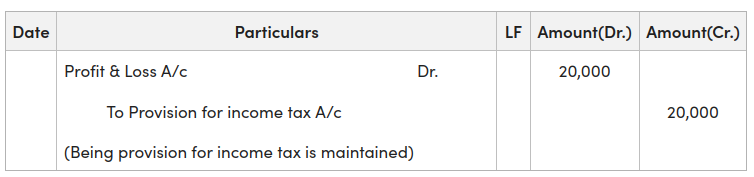

Provision for income tax is to be maintained for ₹20,000. Record the necessary journal entry.

Provision for depreciation is to be maintained amounting to ₹8,000. Record the necessary journal entry.

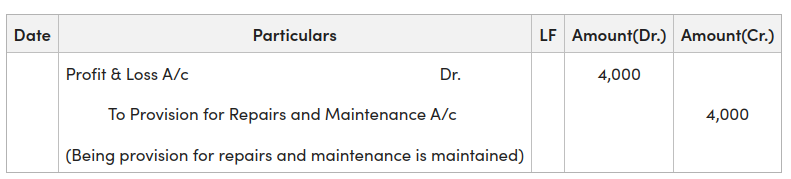

Provision for repairs and maintenance is to be maintained amounting to ₹4,000. Record the necessary journal entry.

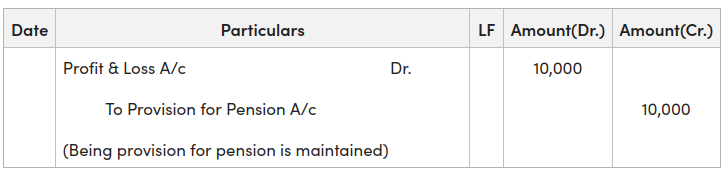

Provision for pension is to be maintained amounting to ₹10,000. Record the necessary journal entry.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}