|

VOOZH | about |

|

VOOZH | about |

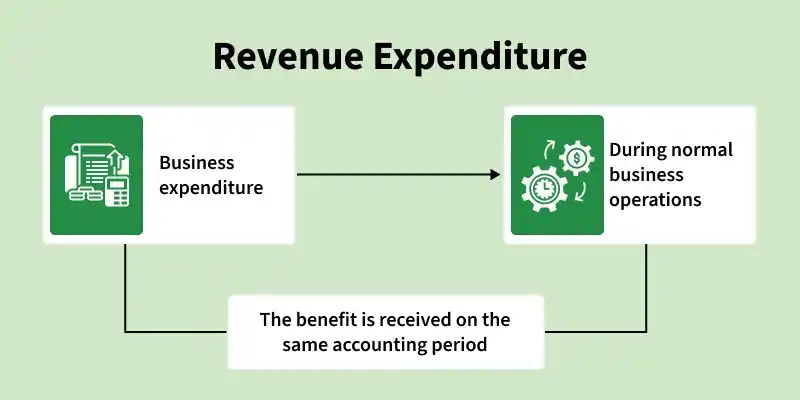

The amount spent whose benefit is either received or exhausted within the accounting period. It can be said that any expense that is not a capital expenditure is a revenue expenditure. Rent, salaries, expenses for maintaining and repairing fixed assets, and so on are examples of revenue expenditures. It also contains the part of capital expenditure that is consumed within an accounting period, like, Depreciation on fixed assets.

1. Direct Expense: The expense that arises from the production of raw material to the final goods/services is known as Direct Expense. For example, shipping costs, electricity bills, commission, factory rent, power, labour wages, etc.

2. Indirect Expense: The expense that indirectly arises through the sale of goods/services and their distribution is known as Indirect Expense. For example, depreciation on machinery, telephone bills, etc.

Revenue Expenditure is shown on the debit side of the Trading and Profit & Loss Account.

Illustration:

Determine which of the following is a Revenue Expenditure:

1. Factory Rent of 1,000.

2. Repairs for 2,000 necessitated by negligence.

3. Wages paid for the installation of new equipment.

4. Salary given to employees.

5. Purchased Patents for 2,00,000.

Solution:

1. Factory rent is a Revenue Expenditure because it is made to run the business. It will be shown on the debit side of the Trading Account.

2. Repairs for 2,000 is a Revenue Expenditure because it is made neither to maintain nor to improve an asset. It will be shown on the debit side of the Profit & Loss Account.

3. Wages paid for the installation of new equipment is not a Revenue Expenditure because it increases the assets of the company.

4. Salary given to employees is a Revenue Expenditure because it is made to run the business. It will be shown on the debit side of the Profit & Loss Account.

5. Purchase of patents for 2,00,000 is not a Revenue Expenditure because it results in an increase in intangible assets of the company.

{kind=link}

{kind=link}