|

VOOZH | about |

|

VOOZH | about |

The movement of cash & cash equivalents or inflow and outflow of cash is known as Cash Flow. Cash inflows are the transactions that result in an increase in cash & cash equivalents; whereas, cash outflows are the transactions that result in a reduction in cash & cash equivalents. Hence, a statement showing flows of cash & cash equivalent during a specified time period is known as a Cash Flow Statement. The transactions of a cash flow statement are categorised into three activities; namely, Cash flow from Operating Activities, Cash flow from Investing Activities, and Cash flow from Financing Activities. Besides the main items of the three activities, there are some other special items that are covered under a Cash Flow Statement.

Sometimes a company purchases a continuing business with its fixed assets and current assets. In this case, the purchase consideration is paid through the Issue of Shares and Debentures. For this, the following procedure is adopted by the company while preparing its Cash Flow Statement:

The valuation of the Stock of a company affects its net profit. Sometimes the stock is valued below cost, which is known as Under Valuation of Stock, and sometimes the stock is valued above cost, which is known as Over Valuation of Stock. While preparing the cash flow statement for these valuations, the following points are taken into consideration:

While preparing a Cash Flow Statement, an increase in the non-current assets of an organisation is treated as a Purchase of Asset; however, a decrease in the non-current assets is treated either as a Sale of Asset or Depreciation on Asset (it depends on the nature of the asset and the amount decreased in the asset). If the amount decreased is more than 10% of the cost of assets (for Furniture), or if it is more than 10% and 25% of the cost of assets (for Building and Plant & Machinery respectively), then it is considered as a Sale of Non-current Assets, instead of Depreciation.

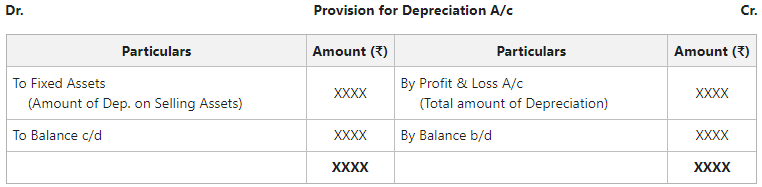

However, there are sometimes certain adjustments or transactions of purchase and sale of office assets that are given after two balance sheets. In those cases, it is essential to prepare accounts related to those fixed assets and provision for depreciation account. And the working of such accounts will be:

i. To find out the cost of fixed assets purchased, when there is no information regarding depreciation:

For Example: From the extracts of the Balance Sheet of Shreya Ltd.

Opening balance of Land and Building ₹80,000. Closing balance of Land and Building ₹1,20,000. Also, there is no information regarding depreciation. Prepare Land and Building A/c.

Solution:

ii. To find out the cost of fixed assets purchased, when the amount of depreciation is given:

For Example, From the extracts of the Balance Sheet of Vanshika Ltd.

Opening Balance of Land and Building ₹1,00,000. Closing Balance of Land and Building ₹1,60,000. Depreciation for the year ₹20,000. Prepare Land and Building A/c.

Solution:

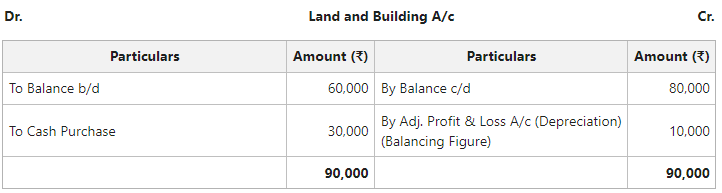

iii. To find out the amount of depreciation when information regarding the additional purchase of an asset is given:

For Example, From the extracts of the Balance Sheet of Shradha Ltd.

Opening Balance of Land and Building ₹60,000. Closing Balance of Land and Building ₹80,000. Purchase of Land and Building during the year ₹30,000. Prepare Land and Building A/c.

Solution:

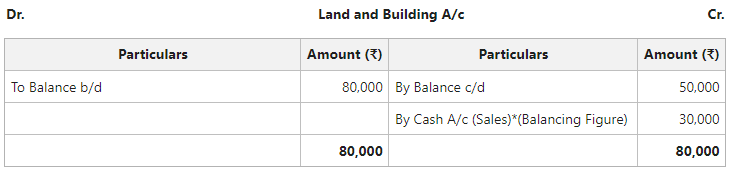

iv. To find out the sale value of fixed assets, when there is no information regarding depreciation:

For Example, From the extracts of the Balance Sheet of Tarun Ltd.

Opening Balance of Land and Building ₹80,000. Closing Balance of Land and Building ₹50,000. No further information regarding depreciation is given.

Solution:

* If the difference between the opening and closing balance of Land and Building (₹30,000) is considered as Depreciation instead of Sales, then, in that case, the ultimate effect on the cash flow statement will be the same. It is because if the amount is considered as Sales it will be recorded as a source of cash, and if it is considered as Depreciation it will be shown on the debit side of Adjusted Profit & Loss A/c and by this amount Cash from Operations in Operating Activities will be increased.

v. To find out the cost of a fixed asset purchased, when the opening balance of the asset, closing balance of the asset, depreciation for the year, and profit or loss on assets sold are given:

For Example, From the extract of the Balance of Stacy Ltd.

Opening Balance of Land and Building ₹1,25,000. Closing Balance of Land and Building ₹1,50,000. Depreciation during the year excluding the Assets Sold is ₹5,000. During the year Land and Building costing ₹10,000 (accumulated depreciation ₹2,500) is sold for ₹6,000.

Solution:

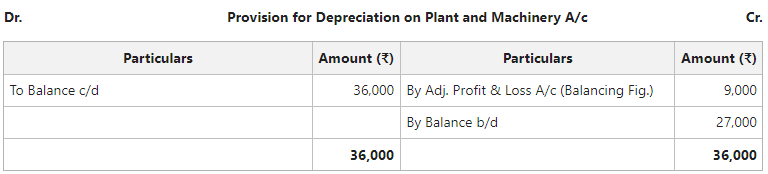

i. To find out the cost of assets purchased when opening and closing balances of asset are given and opening and closing balances of provision for depreciation are given in adjustment.

For Example, From the extracts of the Balance Sheet of Prayag Ltd.

Provision for depreciation on Plant & Machinery stood ₹27,000 on 31st March 2020 and ₹36,000 on 31st March 2021. Find out the Cost of Assets Purchased and Depreciation during the year.

Solution:

Note: In the above example, the opening and closing balances of Plant and Machinery are not shown; instead the balance is shown after depreciation. Therefore, to determine the opening and closing balances of Plant and Machinery, we have to add opening and closing balance of provision to the opening and closing balances of Plant and Machinery, respectively.

ii. To find out the cost of the asset purchased, when the opening and closing balance of the asset (before depreciation), the opening and closing balance of provision for depreciation and profit on the sale of the asset is given:

For Example, From the extract of the Balance Sheet of Nisha Ltd.

Additional Information: A Machinery costing ₹5,000 (accumulated depreciation₹3,000) is sold for ₹1,250. Find out the total amount of depreciation and cost of Machinery purchased.

Solution:

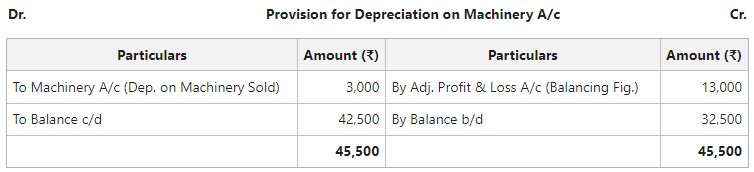

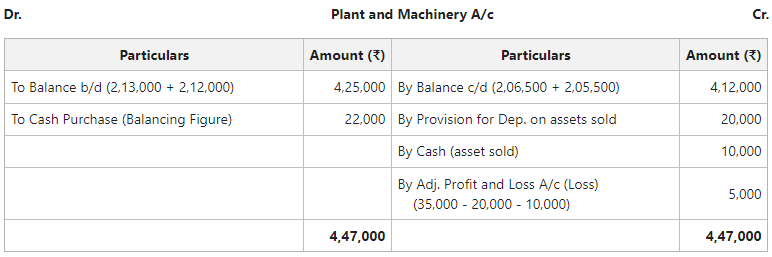

iii. To find out the cost of assets purchased when the opening and closing balance of asset, opening and closing balance of provision for depreciation, depreciation for the year, and gain or loss on asset sold is given:

For Example, From the extract of the Balance Sheet of Vidya Ltd.

The Plant and Machinery for 2019 and 2020 are 2,13,000 and 2,06,500 respectively.

Additional Information: Provision for Depreciation on Plant and Machinery amounts to ₹2,12,000 as on opening balance and ₹2,05,500 as the closing balance. Depreciation for the year is ₹13,500. A machine was sold for ₹10,000 at the time of sale. The net book value of the machine was ₹15,000 (cost ₹35,000 and accumulated depreciation ₹20,000). Find out the cost of the asset purchased.

Solution:

Goodwill is an intangible asset, and its value can increase or decrease. If the value of Goodwill increases, it will be considered as purchase of goodwill and will be treated as utilisation of cash under Investing Activities. However, if the value of Goodwill decreases, it means the company is writing off the goodwill and the amount of decrease will be added to the profit.

Profit before Tax is used as a base for the calculation of cash received from operating activities. However, if Profit after Tax is given, then it is converted into Profit before Tax by adding Provision for Taxation and Provision for Dividends.

Cash equivalents of a firm are extremely liquid investments and can be readily converted into cash with little or no risk of change in their values. Therefore, all the investments whose maturity period is too low (3 months or less) will be included in cash equivalents.

Note: A company does not keep Cash Equivalents with the motive of investment.

Some examples of Cash Equivalents are as follows:

1. Items to be added to the total of Operating, Investing, and Financing Activities:

2. Items to be Deducted:

3. Other Matters:

Kindly refer to Treatment of Special Items in Cash Flow Statement for accounting treatment of more special items in Cash Flow Statement.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}