|

VOOZH | about |

|

VOOZH | about |

The accounting process concludes with the preparation of financial statements. These statements provide information about the financial position and performance of a company. The primary objective of preparing financial statements is to present a true and fair view of the organization's financial performance and financial position. Accounting data is summarized in a systematic manner so that the profitability and overall financial health of the business can be clearly understood. Financial statements also serve as an important source of information for all stakeholders associated with the firm, such as investors, creditors, management, and regulatory authorities. To ensure consistency, reliability, and comparability in financial reporting, these statements—including the Income Statement, Balance Sheet, and Statement of Cash Flows—are prepared in accordance with established accounting principles, standards, and conventions.

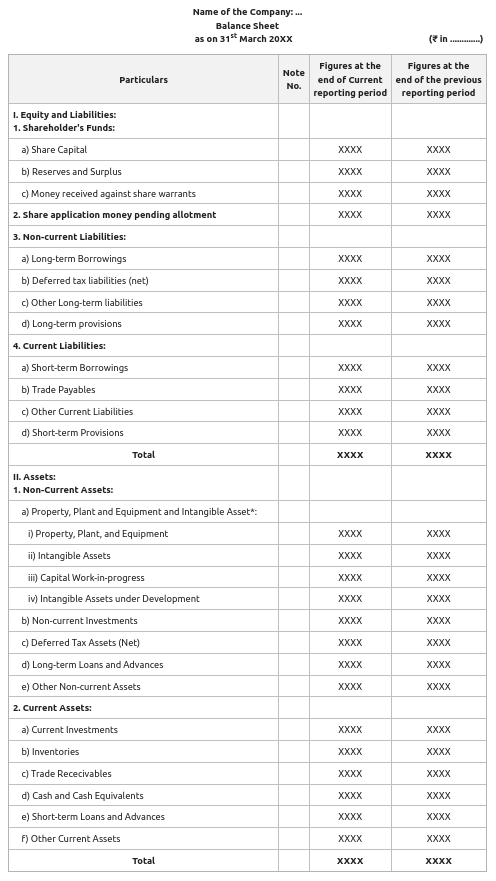

The Balance Sheet of an organization is a financial statement that presents its financial position on a specific date. It shows the value of the organization's assets, liabilities, and capital (or shareholders’ equity) at the end of the accounting period. The Balance Sheet provides a snapshot of what the business owns and owes, as well as the owners’ interest in the business. It is prepared at the end of the accounting year after the preparation of the Statement of Profit and Loss Account and helps stakeholders assess the financial strength and stability of the organization.

Note:

1. The total of each of the sub-items of Equity and Liabilities is directly written in the Balance Sheet, and its detail is shown in Notes to Accounts.

* According to Schedule III of the Companies Act, 2013, the term "Fixed Assets" is replaced with Property, Plant, and Equipment, and Intangible Assets, and "Tangible Assets" by Property, Plant, and Equipment.

1. Shareholder's Funds:

(A) Share Capital: Under this head, some of the important items are:

The disclosure of Share Capital in the Balance Sheet is limited to the following items:

Notes to Accounts:

Note:

1. Equity Share Capital and Preference Share Capital are to be shown separately.

2. If the question doesn't say anything about authorised/issued capital, it has to be shown in the notes to accounts. However, no figures will be shown as shown above.

(B) Reserve and Surplus: Under this head, the following items are shown:

Securities Premium Reserve will be used to write off the items mentioned under Section 52 of the Companies Act 2013 and the balance, if any, will be shown under this head.

Notes to Accounts:

According to Section 52 of the Companies Act, 2013, the amount of Securities Premium can be used for the following purposes:

Notes to Accounts:

(C) Money received against Share Warrants**: A financial instrument that is issued by a public company and gives the holder of the share, the right to acquire a certain number of equity shares specified therein at a later date. The amount received against share warrants is shown in shareholder's funds as on a specified date, these will be converted into equity shares at a pre-determined price. However, the warrants are not shown as a part of the share capital but as a separate line item.

2. Share Application money pending allotment**:

If a company has issued shares, but the date of allotment of shares falls after the date of the Balance Sheet, the application money pending allotment of such shares will be shown in the following way:

3. Non-current Liabilities:

A liability that is not classified as a current liability is a non-current liability. A liability is considered a non-current liability if it satisfies any one of the following conditions.

Therefore, every liability which is not classified as current liability shall be classified as non-current liability.

4. Current Liabilities:

(A) Short-term Borrowings: It includes Loans repayable on demand from banks and other parties, Loans and Advances from Related Parties, Deposits, etc.

(B) Trade Payables: It refers to the amount due on the account of goods purchased or services received by the company in the normal course of business.

(C) Other Current Liabilities: These include Unpaid Dividends, Income Received in Advance, Interest Accrued and due/not due on Borrowings, Calls in Advance and interest thereon, etc.

(D) Short-term Provisions: Every provision for which the company expects that their related claims will be settled within 12 months after the reporting period is included under Short-term Provisions. For example, Proposed Dividend, Provision for tax, Provision for Doubtful Debts, etc.

1. Non-current Assets:

(A) Property, Plant and Equipment, and Intangible Assets: The assets which are held by the company for increasing its earnings instead of the purpose of sale are included under this head. These assets are used by the company for a long time to earn profit and are categorised as follows:

(B) Non-current Investments: Investments that are held for the purpose of retaining them and not reselling are covered under this head. These are classified into two categories; viz., Trade Investments and Other Investments. Trade Investments are those investments that are made by the company in shares or debentures of other companies for the promotion of its own trade and business. Other Investments are those investments that are not trade investments. The investments are classified in the Balance Sheet under the heads:

(C) Deferred Tax Assets (Net): It consists of all the deferred tax assets, including the balance of Deferred Tax Liabilities (Net), which gets converted into Deferred Tax Assets (Net).

(D) Long-term Loans and Advances: The loans and advances which are expected to be received back in cash or kind; i.e., in the form of assets after the period of the Operating Cycle from the date of the Balance Sheet or after 12 months. These are classified into two categories:

(E) Other Non-current Assets: All the non-current assets that do not fall in any of the above four mentioned heads and their sub-heads are included in Other Non-current Assets. These are classified into four categories as follows:

2. Current Assets:

(A) Current Investments: Investments that are held for the purpose of converting them into cash within a short period; i.e., within 12 months from the date of purchase of investment are covered under Current Investments. The investments are classified in the Balance Sheet under the heads:

(B) Inventories: The stock held by the company for the purpose of trade in their ordinary course of business is covered under Inventories. In simple terms, stock held for manufacturing or trading goods and converted into Cash and Cash Equivalents within a short period are classified as Current Assets. It consists of Work-in-Progress, Raw Materials, Finished Goods, Stock-in-Trade, Loose Tools, etc.

(C) Trade Receivables: The amount receivable against the sale of goods or services that are rendered by the company in their normal course of business are covered under Trade Receivables. If the amount is receivable within a period of 12 months or within the period of the Operating Cycle from the date of the Balance Sheet, they are shown as current assets. Trade Receivables of a company consist of both Debtors and Bills Receivable.

Provision for Doubtful Debts: It is a provision made by the company to meet the expected loss of bad debts of a company. It is shown under the relevant head separately and leads ti two approaches as follows:

- The first approach is to show the amount of Provision for Doubtful Debts as Provision under either Long-term Provisions or Short-term Provisions depending upon the duration of Trade Receivables.

- Second approach is to show the amount of Provision for Doubtful Debts by deducting it from the amount under Trade Receivables.

(D) Cash and Cash Equivalents: According to Schedule III, Cash and Cash Equivalents can be classified as:

(E) Short-term Loans and Advances: The loans and advances, which are expected to be realised within 12 months or the period of the Operating Cycle from the date of the Balance Sheet, whichever is more.

(F) Other Current Assets: All current assets which do not fall under any of the above-mentioned heads and sub-heads, come under Other Current Assets. For example, Accrued Income, Prepaid Expenses, Advance Taxes, etc.

3. Contingent Liabilities and Commitments:

(A) Contingent Liabilities: The liabilities which may or may not arise because of their dependency on the event happening in the future are known as Contingent Liabilities. For example, if there is a claim filed against the company in court, then the court may hold the company innocent or guilty. Now, the liability of the company depends on the court's order. Therefore, it is a contingent liability. Besides, the Proposed Dividend is also shown as a contingent liability of the company because it depends upon the approval of shareholders, who may or may not reduce the amount of dividend to be paid [AS-4 (Revised)].

Note: Contingent Liability is not shown in the Books of Accounts of the Company. However, it is disclosed in Notes to Accounts to provide information to the users. It is classified into the following:

(B) Commitments: It is the financial commitment made because of the activities agreed to by the company that it has to undertake in the future. Commitments are classified as follows:

Estimated amounts of contracts remaining to be executed on Capital Account and not provided for Uncalled liability on shares and other investments partly paid, and Other commitments (Nature to be specified).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}