|

VOOZH | about |

|

VOOZH | about |

The accounting process concludes with the preparation of financial statements, which provide information about the financial position and performance of a business organization. The primary objective of preparing these statements is to present a true and fair view of the company's financial performance and financial position. Accounting data is summarized in a systematic manner so that the profitability and overall financial health of the business can be clearly understood. Financial statements also serve as an important source of information for various stakeholders, including investors, creditors, management, employees, and regulatory authorities. To ensure consistency, reliability, and comparability in financial reporting, these statements—such as the Income Statement, Balance Sheet, and Statement of Cash Flows—are prepared in accordance with established accounting principles, standards, and conventions.

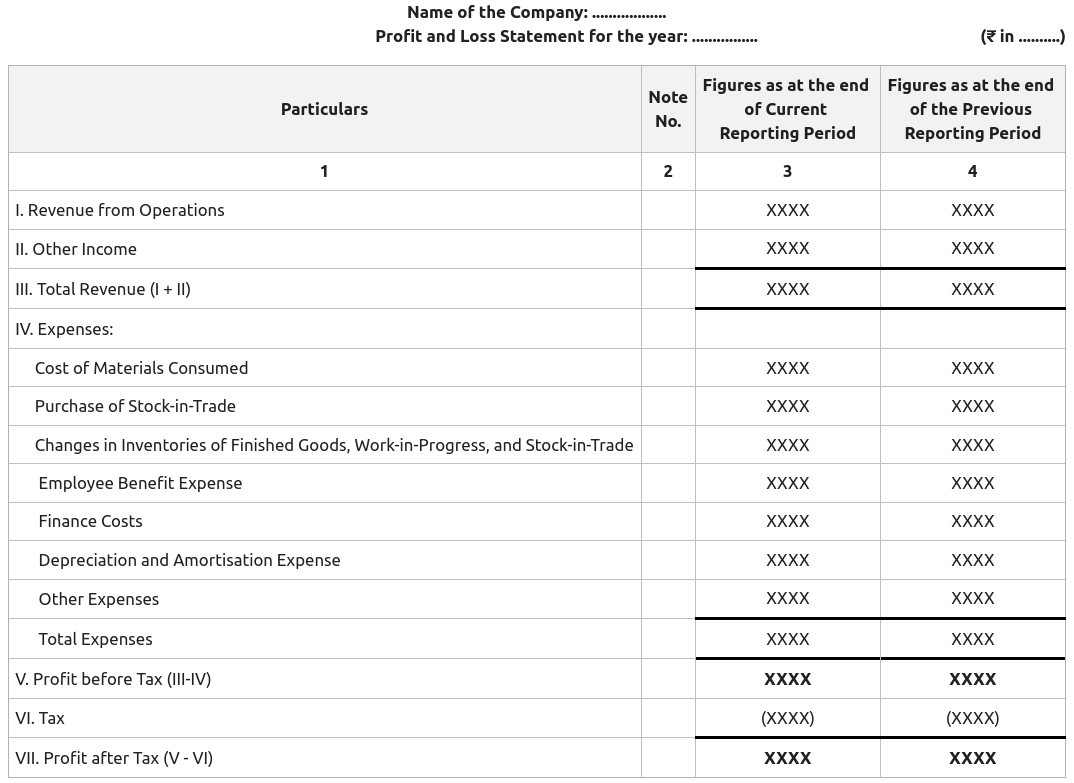

The Profit and Loss Account is a financial statement that helps determine the profit earned or loss incurred by a business during a financial or accounting year. It provides a summary of the organization's revenues and expenses and calculates the net result of its operations in the form of profit or loss. When the total revenues of a business exceed its total expenses, the resulting amount is known as Net Profit. Conversely, when total expenses exceed total revenues, the business incurs a Net Loss. The Profit and Loss Account is prepared using information obtained from the Trial Balance and other relevant adjustments and transactions, enabling stakeholders to assess the operational performance of the organization during the accounting period.

1. Revenue from Operations: Income earned from the main business activities. Examples: Net Sales, Sale of Scrap, Trading Commission, Revenue from Services.

2. Other Income: The revenue that is not earned from business operations comes under Other Income. It is classified under three categories; viz., Rent Received, Interest and Dividend Received, and Net Gain/Loss on the Sale of Investments.

3. Cost of Materials Consumed: = Opening Stock of Materials + Net Purchases - Closing Stock of Materials

4. Purchases of Stock-in-Trade: The Purchases of Stock-in-Trade consist of Net Purchases.

5. Changes in Inventories of Finished Goods, Work-in-Progress, and Stock-in-Trade: = Opening Stock - Closing Stock

6. Employee Benefit Expenses: Consists of Wages, Salaries, Staff Welfare Expenses like Canteen Expenses, and Contributions of Provident Fund, and other staff welfare funds.

7. Depreciation and Amortisation Expenses: It consists of depreciation and amortisation expenses of the company.

8. Finance Costs: Finance Cost is the amount of interest paid by the company on its borrowings.

9. Other Expenses: Other expenses consist of expenses other than the ones that are mentioned above. For example, Telephone Expenses, Selling and Distribution Expenses, Rent and Taxes, Loss on Sale of Fixed Assets/Investments, Advertisement Expenses, Bad Debts, Provision for Bad and Doubtful Debts, and Cash Discount Allowed.

{kind=link}

{kind=link}