|

VOOZH | about |

|

VOOZH | about |

Redemption of debentures refers to the repayment of debentures to debenture holders and the discharge of the company's liability relating to those debentures. Normally, debentures are redeemed on the expiry of the period for which they were originally issued. However, a company may also redeem them before the maturity date, provided such redemption is permitted by its Articles of Association and the terms of issue. Early redemption may be carried out either by paying the debentures in instalments or by purchasing them from the open market.

Redemption out of Profits is a method of redeeming debentures in which a company repays the entire amount of its debentures in one lump sum on the maturity date or earlier, if permitted by the terms of issue. Since debentures represent a loan and are a liability of the company, they must be repaid. Redemption may take place either at par or at a premium according to the terms of issue. Before redeeming the debentures, the company is required to transfer 25% of the face value of the debentures from the Surplus in the Statement of Profit and Loss to a separate account called the Debenture Redemption Reserve (DRR). This transfer reduces the profits available for dividend distribution and reserves funds specifically for the repayment of debentures. Hence, this method is known as Redemption out of Profits.

a. When Debentures are redeemed at Par:

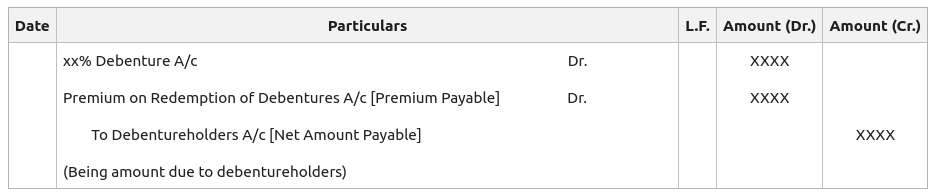

b. When Debentures are redeemed at Premium:

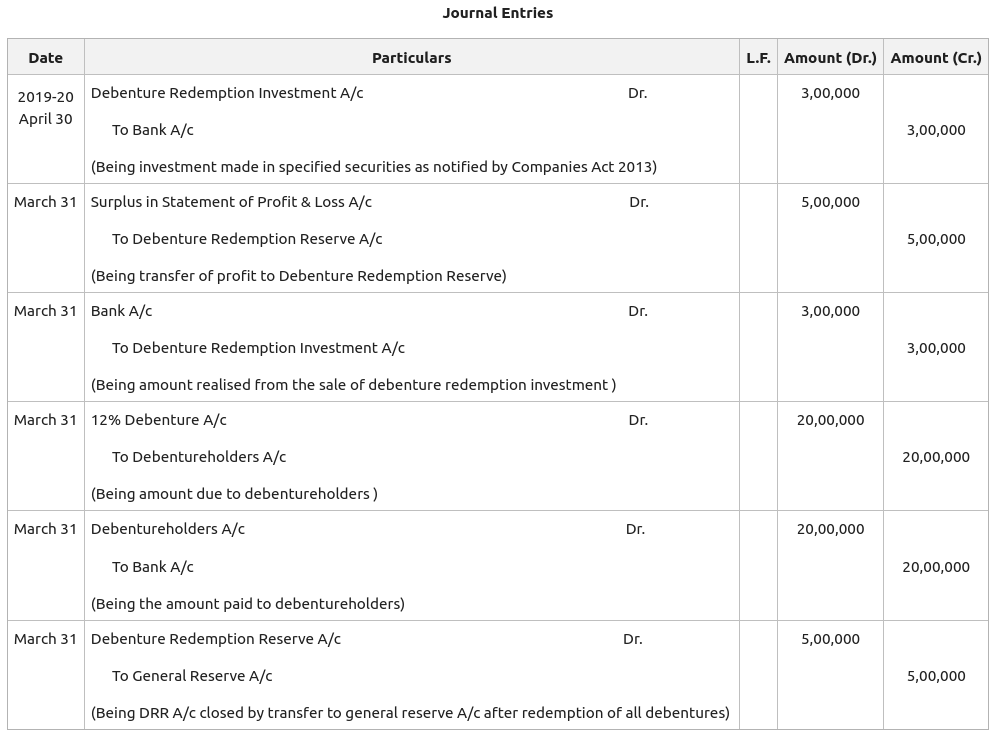

Sahil Ltd. had outstanding ₹20,00,000, 12% Debentures of ₹100 each due for redemption on 31st March 2020. The required investment was made on 30th April 2019. Pass the necessary journal entries regarding the redemption of debentures, creation of DRR, and Investment.

Sukant Ltd. has a balance of ₹21,00,000 in the Profit & Loss A/c. The company decided to forego the payment of dividend and instead utilise the profits to repay ₹15,00,000,12% Debentures (issued on 1st April 2017) fully out of profits on 30th September 2020 at a premium of 10% Debentures. Interest is payable annually on 31st March every year when the accounts are closed. The company also has a balance of ₹10,00,000 in the Debenture Redemption Reserve. Pass the necessary journal entries both at the time of Issue and Redemption of Debentures.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}