|

VOOZH | about |

|

VOOZH | about |

Redemption of debentures is the process of repaying debenture holders and discharging the company's liability arising from the issue of debentures. Generally, debentures are redeemed on the maturity date, that is, at the end of the period for which they were originally issued. However, if permitted by the company's Articles of Association and the terms of issue, debentures may also be redeemed before their maturity. Early redemption can be carried out either through instalments over a period of time or by purchasing the debentures from the open market. This process ensures that the company fulfils its obligation to repay the borrowed funds.

Method in which a company redeems its debentures by buying them back from the stock market. By purchasing its own debentures, the company reduces its liability towards debenture holders, and the purchased debentures are usually cancelled, resulting in their effective redemption. The company may purchase these debentures at par, at a premium, or at a discount, depending on the prevailing market conditions. Such purchases may be made either for immediate cancellation or to hold the debentures as investments for a period of time. Additionally, the company may buy back its debentures either on the due date of interest or on any other date, as per its convenience and financial strategy

Note: In this case, it is assumed that the company has sufficient balance in Debenture Redemption Reserve before initiating the purchase of debentures for cancellation. Therefore, unless it is not stated, it is not required to create DRR under this method. Also, it is assumed that the required investment rate is 15% and it has been made. Therefore, there is no need to make investment.

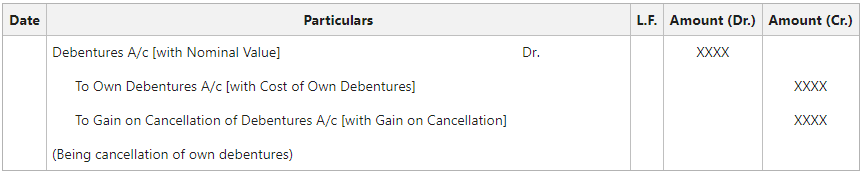

I. On purchase of Own Debentures for Immediate Cancellation:

ii. On cancellation of Own Debentures:

iii. On transfer of Gain on Cancellation:

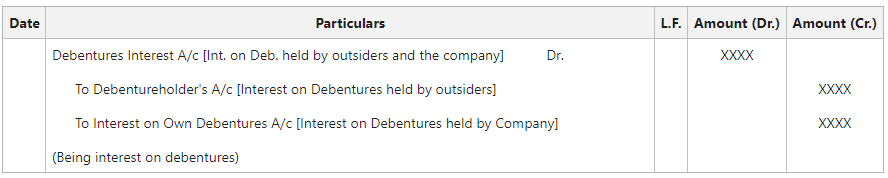

iv. Providing Interest on Debentures:

v. On Payment of Interest on Debentures:

vi. On Transfer of Interest on Debentures to Profit & Loss A/c:

Illustration:

On 1st April 2020, Akanksha Ltd. has 500, 12% Debentures of ₹100 each. On 1st October 2020, the company purchased 150 Own Debentures at ₹93 for immediate cancellation. Interest on debentures is payable half yearly on 30th September and on 31st March. Pass the necessary journal entries on 1st October and 31st March.

Solution:

Working Note:

Profit & Loss A/c =

= 3,000 + 2,100

= ₹5,100

i. On purchase of Own Debentures:

ii. Providing Interest on Debentures:

iii. On payment of Interest on Debentures:

iv. On cancellation of Own Debentures:

v. On transfer of Gain on Cancellation:

vi. On transfer of Interest on Debentures to Profit & Loss A/c:

vii. On transfer of Interest on Own Debentures to Profit & Loss A/c:

Illustration:

On 1st April 2020, Akanksha Ltd. has 500, 12% Debentures of ₹100 each. On 1st October 2020, the company purchased 150 Own Debentures at ₹93 and cancelled on 31st March. Interest on debentures is payable half yearly on 30th September and on 31st March. Pass the necessary journal entries on 1st October and 31st March.

Solution:

i. On purchase of Own Debentures:

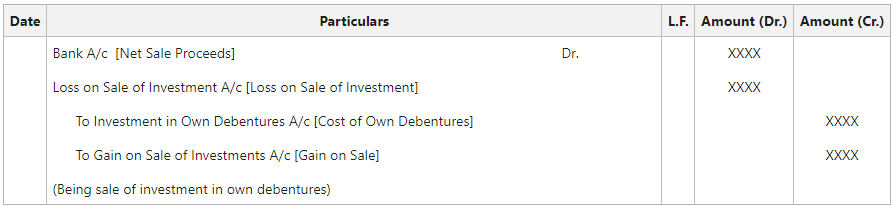

ii. On sale of Own Debentures:

iii. On transfer of Gain on Sale of Investments:

iv. On cancellation of Own Debentures later on:

v. On transfer of Gain on Cancellation:

Illustration:

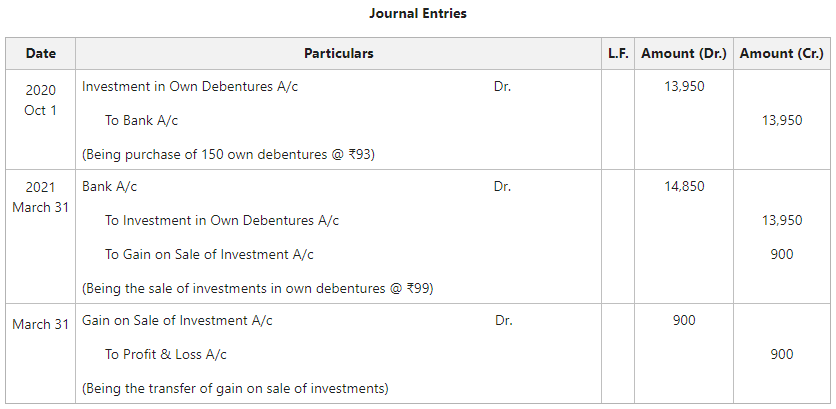

On 1st April 2018, Akanksha Ltd. has 500, 12% Debentures of ₹100 each. On 1st October 2020, the company purchased 150 Own Debentures at ₹93 for investment purpose and sold the same @ ₹99 on 1st March 2021. Interest on debentures is payable half yearly on 30th September and on 31st March. Pass the necessary journal entries on the date of purchases and sale.

Solution:

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}