Thanks @DavidBeckworth for having me on @Macro_Musings. What a privilege

Interested in the global macroeconomics of stablecoins and crypto adoption? Check out our discussion

Link:

Did China really sell $300B since 2021? Unlikely. The sharp rise in rates lowered UST valuations dramatically

Much of the reported decline in China’s UST holdings reflects a drop in UST valuations, not sales. We can do a lot better by looking at the val-adjusted data

1/8

"Maybe China is behind the rise in US long rates...China has fewer dollars to recycle into Treasuries. In fact, China has been selling $300bn in Treasuries since 2021, and the pace of Chinese selling has been faster in recent months," selling $40bn since April: Apollo's Slok

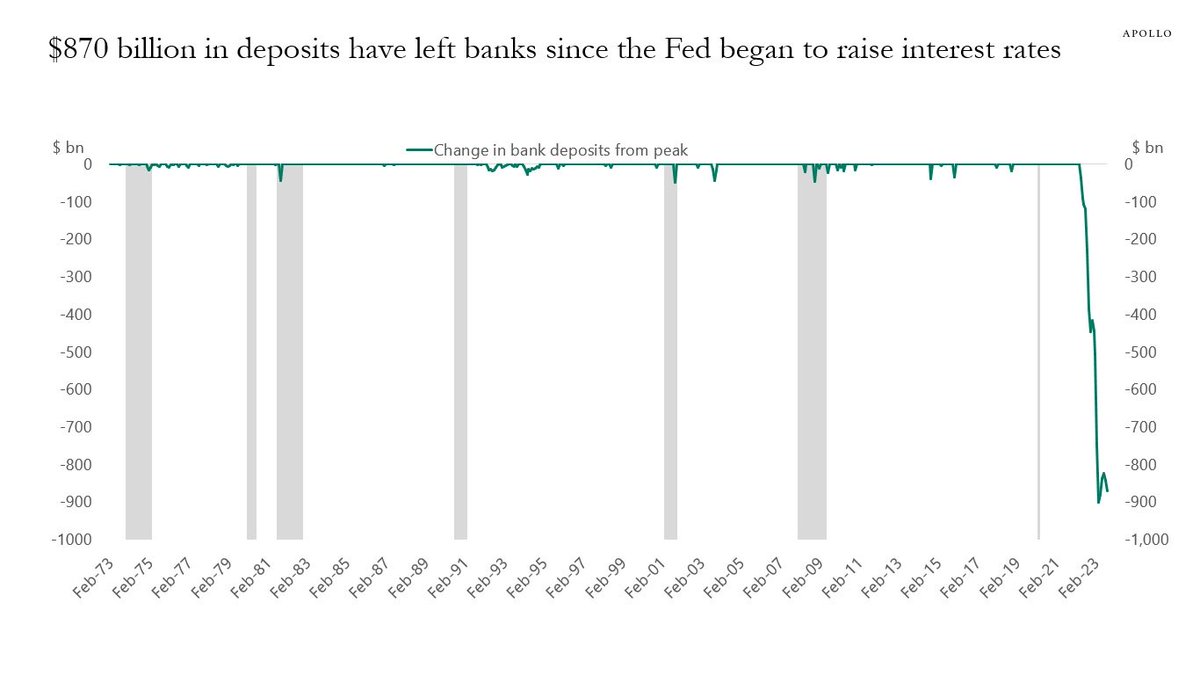

Aggregate deposits can decline for a couple of reasons but deposit flight isn’t one of them. Deposit flight redistributes deposits but doesn't reduce them

This fallacy is gaining momentum on Fintwit so let me offer a quick take on what drives aggregate bank deposits

1/12

Since the Fed started raising rates, a record $870 billion of deposits have left US banks.

This is by far the biggest deposit flight in US history and it’s not even close.

That’s nearly $73 billion PER MONTH or $2.5 billion PER DAY.

Needless to say, why keep your money in a

Took 4+ years but glad to see all my PhD dissertation chapters published! Interested the global macro implications of monetary and financial shocks?

CH1 tldr; US rates propagate to foreign rates differently in countries w managed floats

Link:doi.org/10.1016/j.jimo…

1/3

It’s hard to pin down a single reason explaining the ‘contradiction’ of a prolonged yield curve inversion + prevailing economic conditions

Fwiw @UBS argues there are at least ten:

Check out Figure 5 from @stevehouf's interesting paper:

Larger supply of US Treasuries is significantly associated with higher bond yields when stock-bond correlations aren't negative

Apparently some “gauge of bond term premium just turned positive for the first time since 2021”. Feels like it’s a good opportunity to share my PhD research from 2018, which I worked this “random topic” of what happens if the Fed unwinds its balance sheet. dropbox.com/s/h5jvh62vf8al…

1/x Are some banks no longer in an 'ample reserves' regime? Some data suggests bank funding is under pressure, a narrative recently picked up by the media. But it remains to be seen whether the narrative becomes problematic or not. Some thoughts/data..

So glad to see this in print! Timely w debates over foreign demand for dollars, FX intervention risks and de-dollarization

We shed light on a classic issue that while intuitive has traditionally been difficult to quantify: The effects of FX reserves on exchange rates

1/9

Macro and finance nerds: IMF's global financial stability report just dropped and covers tons of recent market developments w/ great analytics, data etc

link: imf.org/en/Publication…

1/x With 10s2s hitting -80bps, lots of talk on *deeper* inversions leading *deeper* recessions. But no evidence. So I ran the numbers and here's what I found

(Tldr; the *size* of YC inversions don't matter for recession prediction. What matters: whether inversion occurs or not)

The bond market seems to be signaling that the Fed is making a serious mistake. At -80 basis points (as measured by the 10 year vs 2 year Treasury yields), the yield curve is more inverted now than at any time since the early ‘80s when double-digit inflation was entrenched.

1/x With rates soaring and Fed QT, who's buying Treasuries? Foreign investors, US households and Hedge funds

The just-released 2022Q3 quarterly flow of funds is lagged but valuable since it adjusts sector-specific asset flows for valuation changes - which have been huge

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}