|

VOOZH | about |

|

VOOZH | about |

Augmented Dickey-Fuller (ADF) test is a statistical test in time series analysis used to determine whether a given time series is stationary. A stationary time series has constant mean and variance over time, which is a core assumption in many time series models, including ARIMA.

In time series modeling, stationarity ensures that the model's performance is consistent over time. Non-stationary data can produce misleading forecasts and incorrect inferences. That’s why one of the first steps in time series analysis is testing for stationarity and that's where the ADF test comes in.

The Augmented Dickey-Fuller test is an extended version of the Dickey-Fuller test. It tests the null hypothesis that a unit root is present in a time series sample. The presence of a unit root means the series is non-stationary.

The ADF test uses the following regression model:

If the test statistic is less than the critical value, we reject the null hypothesis, concluding the series is stationary.

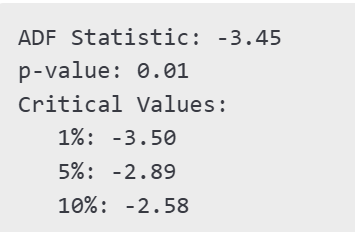

Output:

Since -3.45 < -2.89 (5% level), and p-value < 0.05, the series is likely stationary.

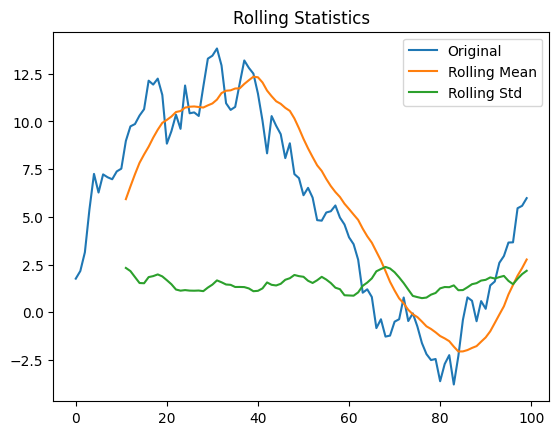

Visual inspection can help support ADF results. You can visualize the rolling mean and standard deviation:

Output

Test Name | Handles Trends | Handles Seasonality | Notes |

|---|---|---|---|

ADF | Yes | No | Most commonly used test |

KPSS | Yes | No | Null hypothesis: stationary |

Phillips-Perron | Yes | No | More robust to heteroskedasticity |

If the ADF test shows that a series is non-stationary, apply transformations:

{kind=link}

{kind=link}

{kind=link}