|

VOOZH | about |

|

VOOZH | about |

The effectiveness of a machine learning model is measured by its ability to make accurate predictions and minimize prediction errors. An ideal or good machine learning model should be able to perform well with new input data, allowing us to make accurate predictions about future data that the model has not seen before. This ability to work well with future data (unseen data) is known as generalization. To consider how well a machine learning model learns and generalizes to new data, we are going to examine the concept of overfitting which is the key factor that can significantly impact the performance of machine learning algorithms on future data, and also going to discuss the Regularization concept which will try to avoid overfitting in machine learning.

In this article, we will cover the Overfitting and Regularization concepts to avoid overfitting in the model with detailed explanations.

Table of Content

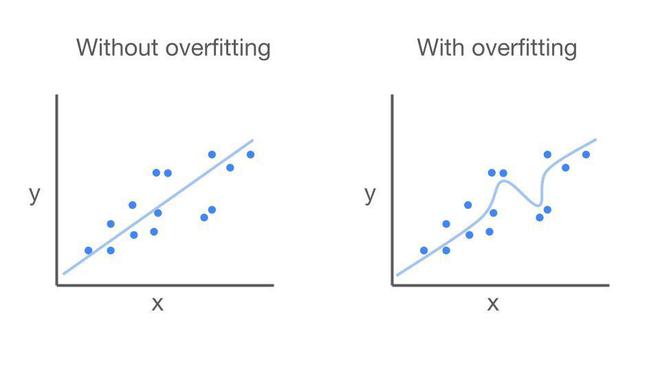

In Machine learning, there is a term called train data and test data which machine learning model will learn from train data and try to predict the test data based on its learning. Overfitting is a concept in machine learning which states a common problem that occurs when a model learns the train data too well including the noisy data, resulting in poor generalization performance on test data. Overfit models don't generalize, which is the ability to apply knowledge to different situations.

Let's walk through an example of overfitting using the linear regression algorithm,

Suppose we are training a linear regression model to predict the price of a house based on its square feet and with few specifications. We collect a dataset of houses with their square feet and sale price. We then train our linear regression model on this dataset. Generally in linear regression algorithms, it draws a straight that best fits the data points by minimizing the difference between predicted and actual values. The goal is to make a straight line that captures the main pattern in the dataset . This way, it can predict new points more accurately. But sometimes we come across overfitting in linear regression as bending that straight line to fit exactly with a few points on the pattern which is shown below fig.1. This might look perfect for those points while training but doesn't work well for other parts of the pattern when come to model testing.

👁 OverfittingThis code performs linear regression using scikit-learn and handles data using pandas. The required modules, such as Lasso, Ridge, and LinearRegression, are imported. The code probably belongs to a machine learning pipeline that splits data, trains a model, and uses mean squared error to evaluate the results.

Load the house dataset from the given link

Output:

Mean Squared Error (MSE) on train data: 681582.53

Mean Squared Error (MSE) on test data: 732229.5

This code uses housing data to do linear regression. It divides the data into training and testing sets after reading the dataset from a CSV file, extracting the input (square feet) and output (indian price) attributes. After that, a linear regression model is built, fitted to the training set of data, and predictions are generated for the testing and training sets. Model performance is gauged by calculating Mean Squared Error (MSE) for both training and testing data. The MSE values are printed at the end. Evaluating the linear regression model's ability to generalize to new data is the aim.

Let's discuss what are the reasons that cause overfitting to the machine learning model which are listed below,

Let's discuss some of the techniques to avoid overfitting to a machine learning model that is listed below,

Regularization is a technique in machine learning that helps prevent from overfitting. It works by introducing penalties term or constraints on the model's parameters during training. These penalties term encourage the model to avoid extreme or overly complex parameter values. By doing so, regularization prevents the model from fitting the training data too closely, which is a common cause of overfitting. Instead, it promotes a balance between model complexity and performance, leading to better generalization on new, unseen data.

Let's discuss about two common techniques that involve in regularization which can prevent model from overfitting

L1 regularization, also known as Lasso (Least Absolute Shrinkage and Selection Operator) regularization, is a statistical technique used in machine learning to avoid overfitting. It is used to add a penalty term to the model's loss function. This penalty term encourages the model to keep some of its coefficients exactly equal to zero, effectively performing feature selection. L1 regularization is employed to prevent overfitting, simplify the model, and enhance its generalization to new, unseen data. It is particularly useful when dealing with datasets containing many features, as it helps identify and focus on the most essential ones, disregarding less influential variables.

Let's derive the mathematical formulation for L1 regularization (Lasso) in simple terms.

In linear regression, the standard model's goal is to minimize the mean squared error (MSE), represented as:

In the above equation, 'y' is the actual target, and 'ŷ' is the predicted target. Now, to add L1 regularization, we introduce a new term to the model's loss function:

Here, 'w' represents the model's coefficients, and 'α' is the regularization strength, a hyperparameter that controls how much regularization is applied. The term Σ|w| sums up the absolute values of all the coefficients.What this additional term does is encourage the model to have some of its coefficients exactly equal to zero. It's like a feature selector it helps the model pick only the most important features, effectively ignoring the less relevant ones.

The larger the 'α' value, the stronger the regularization, and the more coefficients will become zero. This balance between the MSE (model fitting the data) and the Σ|w| term (coefficient sparsity) ensures that the model remains relatively simple and less prone to overfitting while still fitting the data effectively.

Output:

Lasso Regression:

MSE on training data: 680964.93

MSE on testing data: 737817.4

L2 regularization, often referred to as Ridge regularization, is a is a statistical technique used in machine learning to avoid overfitting. It involves adding a penalty term to the model's loss function, encouraging the model's coefficients to be small but not exactly zero. Unlike L1 regularization, which can lead to some coefficients becoming precisely zero, L2 regularization aims to keep all coefficients relatively small. This technique helps prevent overfitting, improves model generalization, and maintains a balance between bias and variance. L2 regularization is especially beneficial when dealing with datasets with numerous features, as it helps control the influence of each feature, contributing to more robust and stable model performance.

Let's derive the mathematical formulation for L2 regularization (Ridge) in simple terms.

In linear regression, the standard model's goal is to minimize the mean squared error (MSE), which is represented as:

Here, 'y' is the actual target, and 'ŷ' is the predicted target.Now, to add L2 regularization, we introduce a new term to the model's loss function:

In this equation, 'w' represents the model's coefficients, and 'α' is the regularization strength, a hyperparameter that controls how much regularization is applied. The term Σ(w^2) adds up the squares of all the coefficients. What this extra term does is encourage the model to keep its coefficient values small. It helps to prevent any one feature from having an overly dominant effect on the predictions. In other words, it adds a cost to having large coefficients.

The larger the 'α' value, the stronger the regularization, and the smaller the coefficients will become. This balance between the MSE (model fitting the data) and the Σ(w^2) term (model's coefficients) ensures that the model doesn't become too complex, preventing overfitting while still fitting the data effectively.

Output:

Ridge Regression:

MSE on training data: 680964.93

MSE on testing data: 737833.98

In conclusion, overfitting is a common challenge in machine learning, where a model becomes excessively tailored to the training data, leading to poor generalization on new data. In simple words it's like memorizing a book but failing to understand the story. To prevent from overfitting, we discussed various techniques, including simplifying the model, gathering more data, and validating model performance. Regularization is a main technique that prevent overfitting by adding a penalty term to the model's loss function. L1 regularization (Lasso) encourages sparsity in coefficients, effectively selecting essential features, while L2 regularization (Ridge) maintains all coefficients small but not zero. These regularization techniques make a balance between model complexity and performance, enhancing generalization to new, unseen data.

{kind=link}

{kind=link}