|

VOOZH | about |

|

VOOZH | about |

Deep learning is transforming the financial industry by enabling institutions to analyze massive, complex datasets, predict market trends, and manage risk with remarkable precision. Unlike traditional models, it leverages layered neural networks to process both structured and unstructured data like news, social media, and historical prices unlocking insights that were previously out of reach. As financial data continues to grow in volume and complexity, deep learning provides powerful tools for algorithmic trading, fraud detection, and portfolio optimization.

The foundations of Deep Learning go back to the development of stochastic gradient descent, which was an early step toward optimizing learning algorithms. However, limited computational power at the time hindered practical application. With advancements in GPUs, distributed systems, data storage, and modern libraries like TensorFlow, Deep Learning has since experienced rapid growth data-intensive sectors like finance and banking.

A core neural network can be represented as :

In financial applications, Y might represent a predicted stock price, credit risk score, or portfolio return. By stacking multiple layers of perceptron, we form deep neural networks (DNNs) capable of modeling intricate relationships.

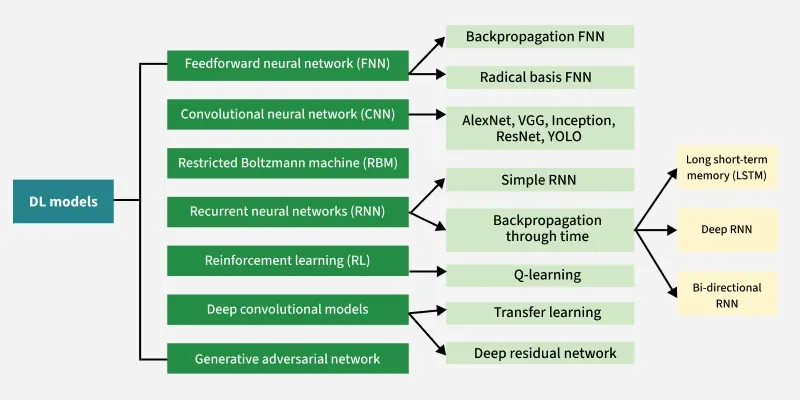

While traditional Neural Networks like MLPs or feedforward networks do not account for temporal patterns, financial data often comes in time series form. To address this, models like recurrent neural networks (RNNs) andlong short-term memory networks (LSTMs) are used. These architectures are designed to capture sequential dependencies, making them ideal for financial forecasting.

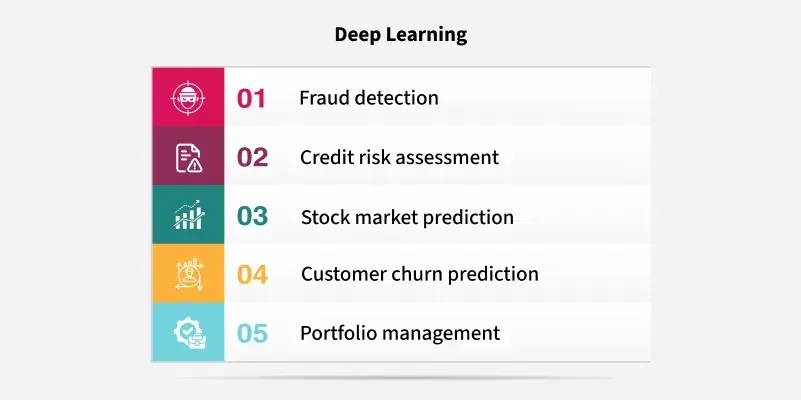

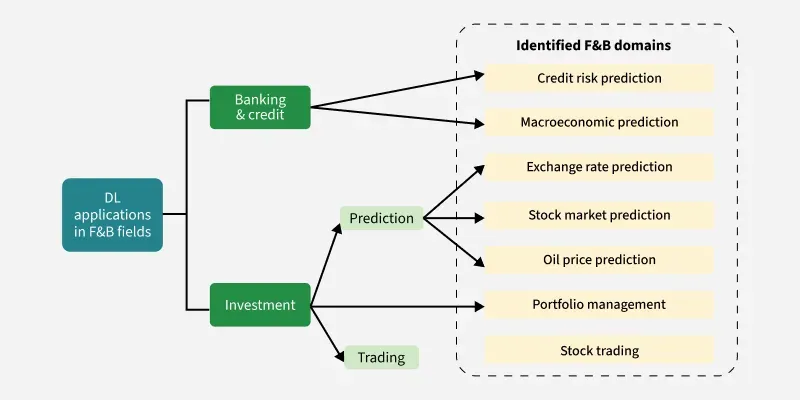

Exchange rate forecasting involves predicting how the value of one currency will change compared to another. This is necessary for international trade, investment, and monetary policy decisions. Deep learning models like Deep Belief Networks (DBNs) can uncover hidden patterns in complex and noisy financial data better than traditional models such as ARMA or SVM. By combining neural networks with tools like chaos theory or optimization algorithms, researchers have developed hybrid models that further improve prediction accuracy.

We aim to forecast future stock prices or market movements based on historical data, news, or investor sentiment. Accurate predictions can help investors make better trading decisions. Deep learning models like CNNs and LSTMs can process large volumes of data like stock prices, trading volumes, and even news articles to detect patterns over time. They can also understand context and sentiment from financial texts, making them more effective than basic machine learning techniques.

Algorithmic and Quantitative Trading involves creating automated systems that buy or sell assets based on mathematical models and data signals, aiming to profit from market inefficiencies. LSTM networks are used for handling time-series data, help in understanding market trends over time. Reinforcement learning (RL)models can simulate trading as a decision-making game, learning strategies by interacting with market data similar to how a human trader would learn from experience.

Our task here is to assess how likely a borrower is to default on a loan, or detecting fraud in financial transactions. Accurate models are key to reducing financial losses for banks. Models like FNN, CNN and LSTM are capable of learning subtle patterns in user behavior or transaction histories that indicate risk or fraud. For instance, LSTMs can spot unusual sequences in credit card usage, while CNNs can pick out important features in a customer’s financial profile, improving credit scoring accuracy.

Portfolio management involves choosing the best mix of investments (like stocks, bonds, etc.) to maximize returns while managing risk. Advanced models like RNNs and RL algorithms can adapt to changing market conditions and learn strategies to balance risk and return. These systems can make dynamic decisions, such as adjusting investments in real time, while accounting for transaction costs and risk preferences.

Macroeconomic Forecasting involves predicting large-scale economic events like recessions, financial crises, or inflation trends. It helps policymakers and financial institutions plan ahead. Deep learning models can process vast and varied datasets like employment rates, GDP, and global news. They can learn patterns that may signal an upcoming economic event. These models have shown higher accuracy than traditional methods like decision trees or logistic regression in anticipating such changes.

Commodity and Price Forecasting refers to predicting the future prices of commodities such as oil, gold. or natural gas, which is important for budgeting, hedging and trading strategies. By combining models like MLPs, wavelet transforms, and SVMs, hybrid deep learning systems can handle the complex, nonlinear trends typical of commodity markets. These models are better at adapting to sudden price shifts or seasonal patterns than conventional forecasting methods.

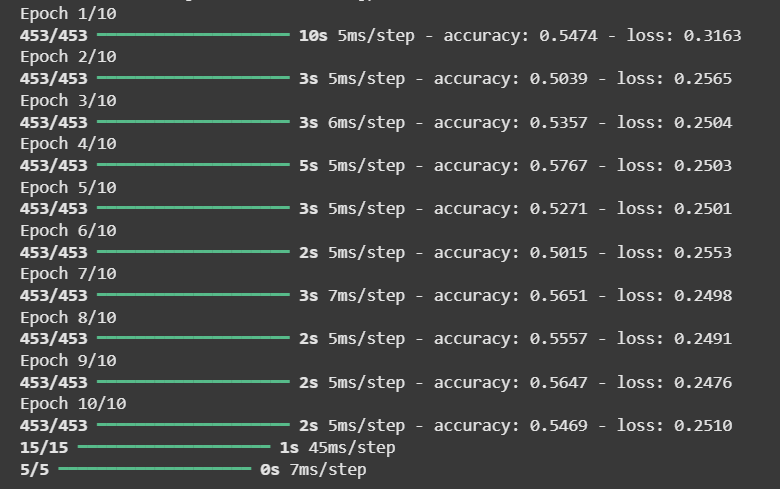

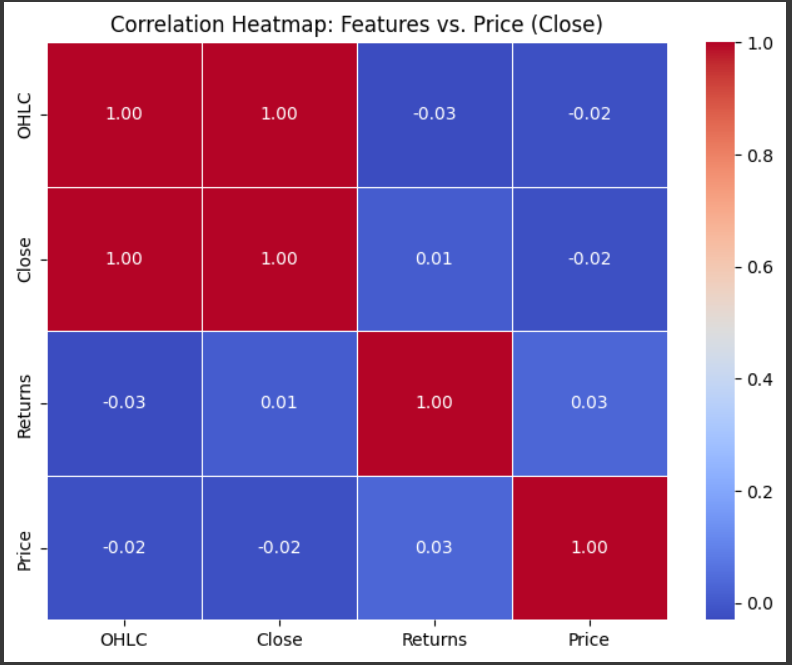

Following example demonstrates a deep learning-based approach to stock trend prediction, using Apple Inc. (AAPL) stock data. The goal is to predict whether the stock price will go up or down the next day, which is a common binary classification problem in quantitative finance. Here we employ a Long Short-Term Memory (LSTM) network to model temporal dependencies in stock prices and trends. A correlation heatmap finally helps in visualizing relationships between input features and the stock price.

We start by importing libraries for data loading, processing, visualization, feature scaling, model building, and evaluation. Yfinance is used to download historical stock data, Keras helps us build the LSTM model.

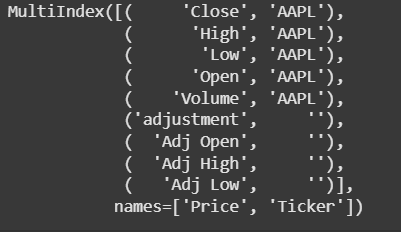

We fetch Apple Inc.'s OHLCV (Open, High, Low, Close, Volume) data from Yahoo Finance.

Output:

As Yahoo already provides adjusted close prices, we simply use a dummy adjustment factor of 1 here. In real cases (like dividends/splits), you would use actual adjustments to normalize values.

The model begins by computing the average of the adjusted Open, High, and Low prices to summarize daily price movement. It then includes the actual Close price to capture end-of-day market sentiment and calculates the daily return as the percentage change from the previous day. These three components are combined to form the feature matrix X, which serves as the input for the deep learning model.

MinMaxScaler.We reserve 75% of the data for training and the remaining 25% for testing.

Features and labels are then separated for both sets.

Output:

Output:

We then calculate and plot the correlation matrix to understand how features relate to the actual stock price. This helps in assessing feature importance or selection in future iterations. Though simple this showcases how LSTM networks can be used to predict stock price trends using historical data. By engineering features like average OHLC values, close prices, and returns, and reshaping the data for sequence learning, a binary classification model is built to forecast market direction. The model demonstrates the potential of deep learning in financial prediction and can be extended with more features and tuning for better performance.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}